Disruptive companies reimagine the landscape of an existing industry or outright give birth to an entirely new industry, allowing the most visionary of disruptors to devour market share and leave competitors in the dust. And not surprisingly, the wealthiest people on the planet tend to create their wealth by concentrating in disruption of precisely this form, either as founders or early investors in the greatest disruptors. But building significant wealth by concentrating in disruptors requires two critical ingredients for success: 1. Accurate identification of disruptors before they are discovered by other investors and 2. Avoiding risk of ruin by over-concentrating one’s wealth into a handful of disruptors. In this blog we review a novel systematic approach for clearing both hurdles towards disruptive wealth generation; we present a first principles research framework for identifying generational disruptors early and then lay out an options strategy that can create strong upside potential without the pitfalls of hyper-concentration.

A Reality Check on Individual Stock Investing

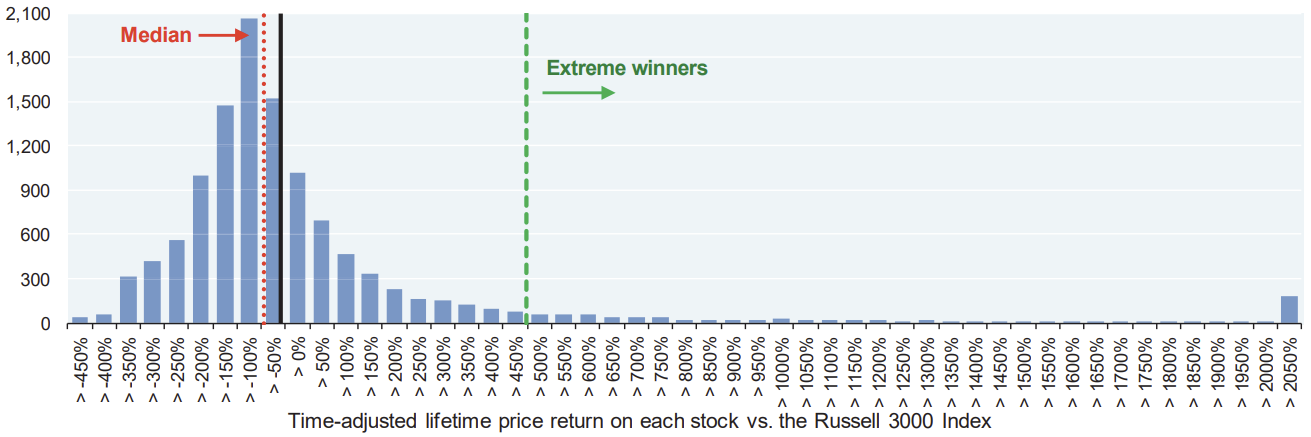

Before we jump into our framework for concentrated investing in disruptors, let’s take a minute to put some data behind our assertions about the upside potential and downside risks of concentrated investing. Figure 1 shows the distribution of excess lifetime returns for each stock that was in the Russell 3000 from 1980 to 2014. On the positive side of investing in individual stocks, one can see the unbelievable upside potential in those names that prove to be the ultimate disruptors, of which we’ve seen around 250 of them in the 25-year sample shown (last histogram bin in graph). On the flip side, 2/3 of stocks over their lifetime had negative excess returns versus the benchmark, with a median excess return of -54% for all names. Additionally, 40% of this universe suffered catastrophic losses that were never recovered, precisely the risk of ruin we mentioned earlier (the definition of unrecoverable losses can be found in the source document for Figure 1). Hence we see the massive potential of investing in the true disruptors, while simultaneously seeing how catastrophic concentrating in just a few names can be. So how can we access the full wealth potential of disruption while mitigating the downside risks?

Figure 1: Distribution of Excess Lifetime Returns of Individual Stocks in the Russell 3000, 1980-2014 Source: J.P. Morgan. https://www.chase.com/content/dam/privatebanking/en/mobile/documents/eotm/eotm_2014_09_02_agonyescstasy.pdf

A First Principles Approach for Identifying Disruptors

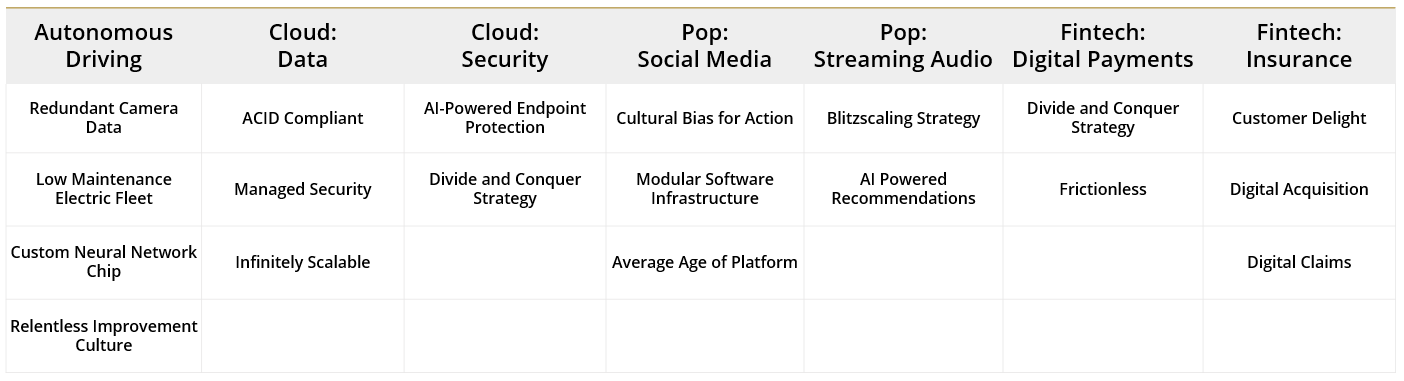

Disruptors can’t be identified early using corporate earnings or other standard metrics deployed in the investment field. Instead, one must take a more scientific, first principles approach to identifying disruptors before they burst onto the scene. To do this, Simplify partners with Volt Equity, a Silicon Valley technology boutique, to carefully analyze new technologies and their ability to disrupt life and business as we know it. Once a disruptive technology has been identified, we then break down the new field into its salient features and identify those companies poised to excel in all necessary disciplines for true disruption. Figure 2 highlights the key pillars that drive true success in a number of key themes we are focused on today. By then analyzing each contender company based on their prowess in each discipline, we can then identify those disruptors most likely to take the lion’s share of the new market.

Figure 2: First Principles Deconstruction of the Most Disruptive ThemesSource: Volt Equity.

An Option Framework for Capturing Upside Without Extreme Concentration

Once disruptors are identified, how can we then build portfolios that provide the upside we want from generational disruption while avoiding the downside of concentration? Enter stock options, that can provide equity-like upside at a fraction of the cost of a full equity investment, precisely the highly asymmetric payoff we need to solve this problem. For example, let’s say you believe Tesla is going to dominate the autonomous driving space for decades to come and you want to capitalize off this dominance. Rather than putting all your money into Tesla directly, one can buy call options on Tesla, which if structured properly can provide the upside of a full investment in the stock (or more), with just a fraction of the cash outlaid and ultimately at risk. Now the exact upside one can capture by swapping stocks for options varies with the option strikes and expiries deployed, so to really understand the full potential of this form of stock/option swap, we need to first decide the precise option structure we would want.

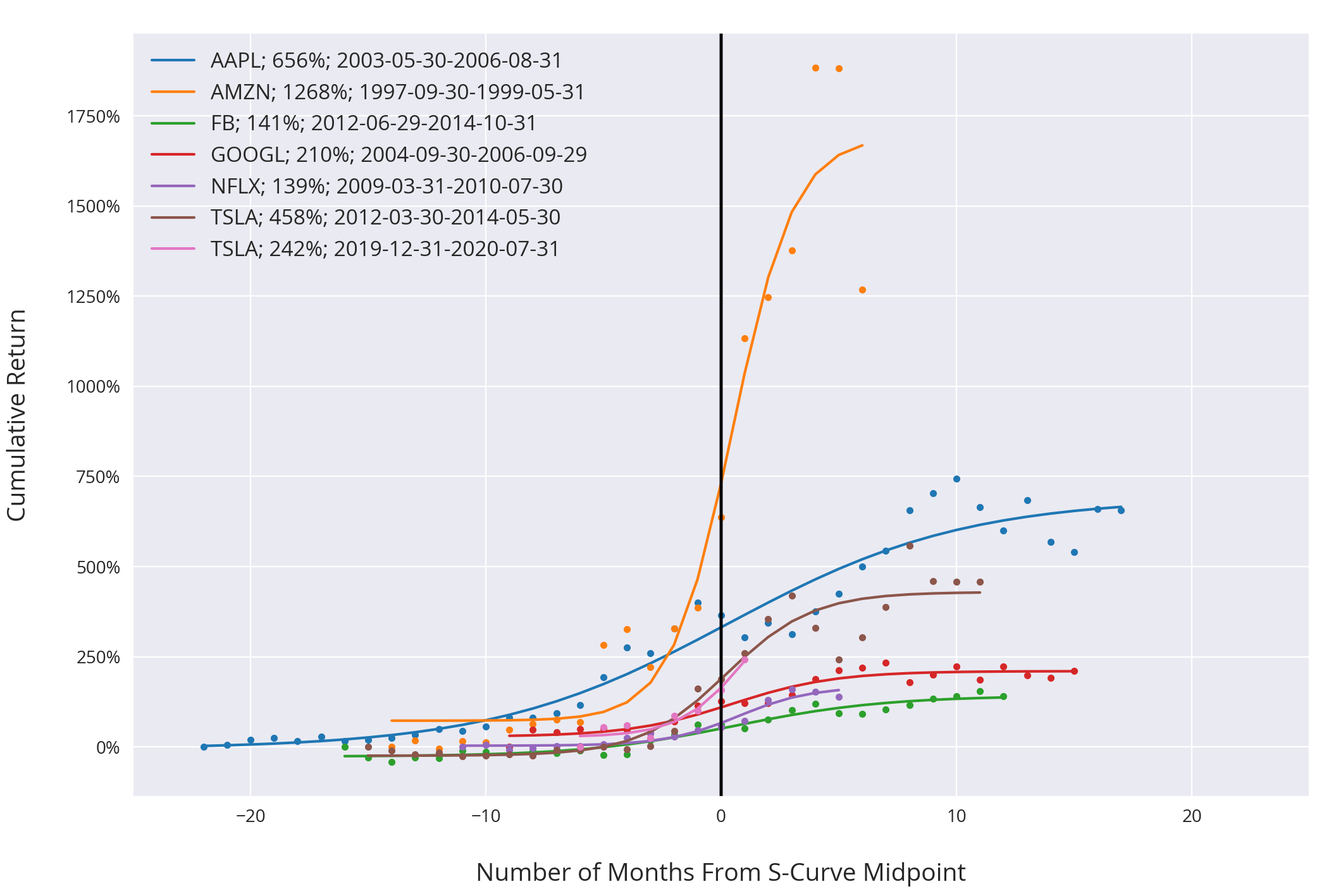

It turns out that disruptive companies typically have a price trajectory that makes the swap from concentrated stock positions to a fractional position in call options very compelling. Figure 3 shows the empirical S-curves for some of the most disruptive companies of the past few decades. There are a few key observations we can quickly make regarding disruptive price trajectories that can help us structure our option exposure to best capture disruptive upside while mitigating concentration risk. The first thing we see is that S-curves typically take about two years to play out, hence we can limit our option expiries to about two years out, which coincidentally is the typical max horizon for listed options. Second, we generally see accelerated growth for around six months in the middle of the full two year S-curve, hence we should ladder in some six month calls to capture those biggest of booms. And finally, we see that disruption is minimally accompanied by a move up of about 100-200%, but can be significantly larger. Given these guide posts, Simplify will deploy a ladder of call options that are 50-100% out-of-the-money, from 6 months to 2 years in expiry, in lieu of a significant stock investment. The exact portfolio weightings to each strike/expiry combo are then actively determined based on the exact timing and magnitude of a company’s next expected S-curve, or if the company is in the middle of an S-curve already, the extent to which the S-curve could continue.

Figure 3: Anatomy of an S-CurveSource: Bloomberg. Calculations by Simplify Asset Management. The results are NOT an indicator of future results. Additional information regarding the construction of these results is available upon request. PLEASE SEE FULL DISCLOSURES BELOW.

Parting Words

The power of concentrating in true disruptors is undeniable. But the challenges of determining the real disruptors and avoiding concentration risk are equally as undeniable. By using a first principles approach to deconstructing disruption into its salient disciplines we believe we can identify true disruptors well ahead of significant market share has been achieved. And by understanding how the price of disruptive companies generally evolves, we can utilize options to help capture their upside potential without taking on concentration risk that can lead to catastrophic loss.