Attractive sources of income are hard to come by today. Bond yields are near all-time lows after 40 years of falling interest rates. Stock dividends are increasingly uninspiring as equities continue their meteoric rise. But not all sources of income have been squeezed away. One attractive source of yield today is the income generated by selling volatility. Yet selling volatility can be risky and years of precious income can be lost quickly.

In this blog we present compelling new ways to manage the specific risks associated with selling volatility. The blog culminates in a new approach for generating income from the volatility premium that systematically mitigates downside risks.

Volatility Premium 101

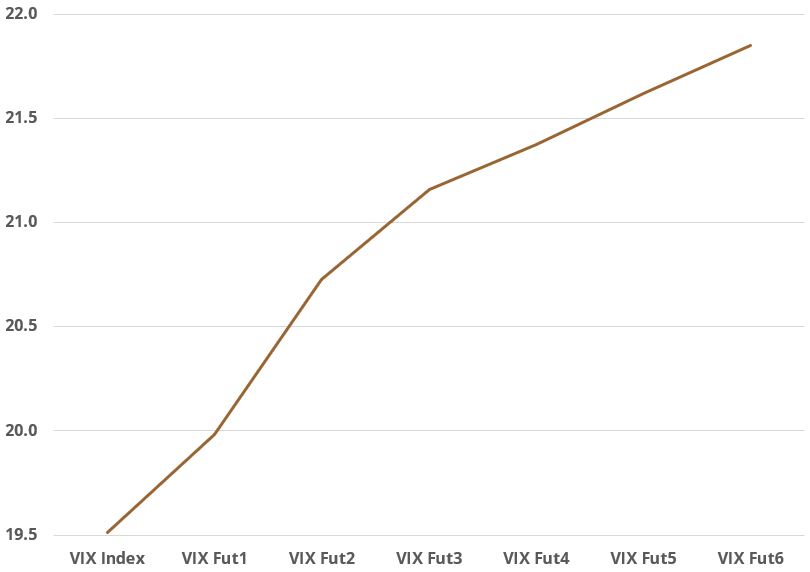

Let’s begin by reviewing what the volatility premium is and how it is harvested. Figure 1 shows the average term structure for VIX spot and the first 6 futures contracts over the past fifteen years. As you can see, the curve is on average in contango, which means the longer-dated futures are higher in price than shorter-dated futures, a consistent structural anomaly that stems from VIX futures being used as a hedge for equities. To harvest this contango premium one simply needs to short the futures contract, typically the front month due to high steepness and liquidity, and continuously do so by rolling the front-month short to the next month, ad infinitum, on a monthly basis. As one may expect, since long positions in VIX are used to hedge equity positions, the VIX curve can indeed spike during equity selloffs, and is the primary risk to harvesting the volatility premium in the manner just described.

Figure 1 – Average VIX Term Structure from 2016 to 2020

Source: Bloomberg

The monthly yield one can receive from this continuous roll of the front-month VIX short as just laid out can be calculated as (VIX 2nd Month – VIX 1st Month)/((VIX 2nd Month + VIX 1st Month)/2), which is approximately 56% annualized for the average term structure presented in Figure 1 (we just multiply the monthly yield by 12, assuming income is distributed monthly). This yield is not static, as both levels and spread between contracts are continuously changing. Over the past 6 months, this yield has in fact been closer to 80%.

Optimal Exposure for Volatility Harvesting

As mentioned, short volatility investments can have massive drawdowns, as was the case in the high-profile implosion of XIV in February of 2018. This blowup was first and foremost due to the fund’s total short VIX exposure -- a 1:1 ratio of VIX short exposure to fund assets -- which created a -100% exposure to VIX. To avoid this kind of blowup, the first thing one should do is reduce the exposure down from -100%. Post “Volmageddon 2018”, the market norm is to sell volatility with a -50% exposure, but is this truly optimal? Figure 2 shows returns for the last fifteen years in short VIX strategies with 50%, 25%, and 12.5% short exposures. The sweet spot, where the annualized return from the trade is optimal, is around 25%. One might expect the 50% exposure to have the highest return. This is true for yield, but not true in terms of compounded annual return. The reason is simple: a 50% drawdown requires a 100% return to get back to even. So even though the yield at 50% exposure is two times the yield for the 25% exposure product, the extra yield is more than offset by the larger drawdowns. Investors looking to capture the volatility premium over extended periods should therefore focus on the “compound optimal” exposure near 25%, rather than the “yield maximizing” exposure near 50%.

Figure 2 – Inverse VIX Strategy Performance as a Function of Exposure (2016 to 2020)Source: Bloomberg

Further Mitigating Downside With Options

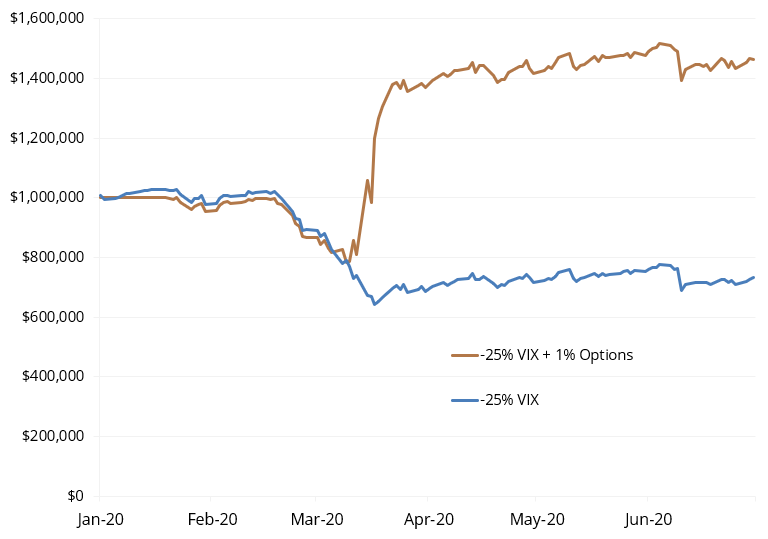

In the previous section, we saw that reducing drawdowns is critical to optimal harvesting of the volatility risk premium. Beyond tuning the total exposure of the trade, we can also consider the direct use of options to help limit downside and improve compound returns. Figure 3 shows the cumulative performance during the COVID-19 crisis of a simple hypothetical strategy that is -25% short VIX and rolls a monthly call option on VXX that is 200% out-of-the-money, spending 1% annually on option premium (1/12th of 1% each month). Also in Figure 3, we see the performance of the -25% VIX strategy without options. The COVID drawdown gets cut in half from the option position, and even at the relatively small 1% annual option budget, we see the options add significant value to the strategy beyond just drawdown protection.

Figure 3 – Downside Mitigation of 25% Inverse VIX Strategy via OptionsSource: Calculations by Simplify Asset Management. The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Hypothetical strategies and indices presented are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request. PLEASE SEE FULL DISCLOSURES BELOW.

Parting Words

Equity hedging imbalances create a structural opportunity to sell volatility. While the yield one can earn in this carry trade is variable, it has produced an incredibly attractive 45% annual yield over the past fifteen years. But this income comes with severe drawdown risk. By addressing this risk head-on, by choosing more optimal short VIX exposure levels and deploying option protection, it is possible to use the volatility premium to create an attractive income source with explicitly managed risk.