Price action across global markets in December has been dominated by the continuing focus on the path for global monetary policy, led by the US Federal Reserve. Global fixed income markets, led by front end interest rates, rallied substantially on December 13th with the Fed’s decision to leave interest rates unchanged. This decision was broadly anticipated, but a revision of the Fed’s “dot plot” lower showing the median forecast of Federal Open Market Committee members to include 3 cuts by the end of 2024 was a dovish surprise. Perhaps even more significantly, Chairman Powell refrained from providing material pushback against recent optimistic price action in November and early December, suggesting that policymakers are willing to accept easier financial conditions. Markets have taken this as confirmation of a substantial dovish pivot and repriced assets accordingly. It is worth noting that in our view the markets are well ahead of the Fed’s dot plot estimates, with short-dated interest rate pricing implying more than 6 cuts by the end of 2024 according to Bloomberg.

The resultant aggressive move lower in short-term interest rates seems to have been counter to most long-term trend indicators, driving some underperformance on short-dated interest rate positions across the managed futures space. However, short-term trend signals were less bearish, which has offset positioning to a degree and reduced the overall performance impact of this month’s bond market volatility on the managed futures space. Meanwhile, an extension of the bullish uptrend in global equities, again in reaction to the perception of a more dovish policy, has also appeared to have helped participants.

The dovish pivot, alongside the continued focus of the Bank of Japan policy, has contributed to a mild ongoing downtrend in the USD. This, in conjunction with concerns about supply chain disruptions arising from recent hostilities of Houthi rebels against Red Sea shipping lanes, has allowed energy markets to reverse mildly higher despite fears of excess supply. Most long-term trend systems again haven’t performed on this price action, though short-term signals may have done better for some participants. In grains and softs meanwhile, long-established market trends did appear to extend, with the exception of Sugar, where changes to onshore regulations in India disallowing the use of cane in ethanol production resulted in a large counter-trend bearish reversal in the price action. Metals, like energy, reversed intra-month on the pivot news but were not strong contributors to trend indicator performance overall.

Looking ahead, in our opinion the monetary policy narrative seems likely to continue to drive price action, with many commentators noting the recent pro-correlated behavior of equity and bond prices, and questioning whether an extreme dovish pivot by the Fed is justified with equities making new highs and ongoing tight labor market conditions. We are expecting extreme price sensitivity of all markets to any information that could revise the market’s expectations for policy rates in a more hawkish direction again. For now, however, trend indicators remain mostly bullish equities and are now more mixed on fixed income, with the recent price action having driven a substantial reduction of bearish signals on global interest rate markets. Long-term trend indicators remain generally bearish on energy and grains, and bullish on softs. We see a more mixed set of indicators on metals. However, with ongoing USD weakness and any extension of the recent week’s rally in metals, we believe we could see indicators move to a more bullish stance from here.

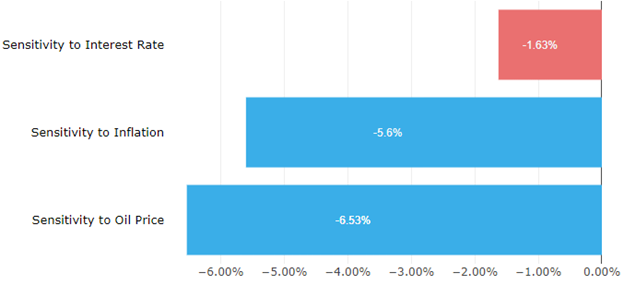

Turning to factor land, Macro Betas gave back much of the gains seen in recent months (see Figure 1). Leading the fall was Sensitivity to Oil Price, which followed the steady decrease in crude oil prices since mid-September. Sensitivity to Inflation and Sensitivity to Interest Rates similarly fell, as headline inflation continues to steadily fall towards the Fed’s 2% target and rate cuts are on the horizon.

Figure 1: Macro Betas gave back much of the gains seen in recent months as inflation, interest rate expectations, and crude oil prices all fell in December

(Returns November 21 - December 20)

Source: Wolfe Research

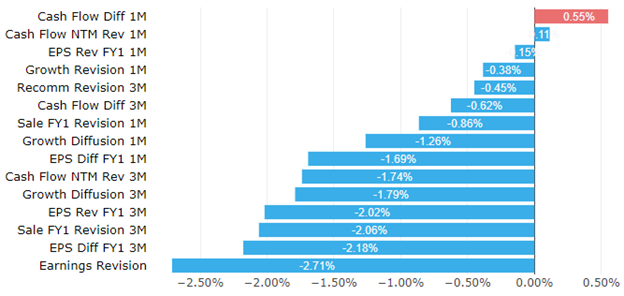

Quant factors also gave back some of the gains experienced recently. However, it is noteworthy that Medium Frequency Quant and High Frequency Quant fell the least, showing there is still a benefit to tracking higher frequency signals in this regime shifting period. As further evidence of markets entering a period of regime shift, Analyst Sentiment factors (see Figure 2) mostly lost in December as well, signaling that sell-side analysts were basing their revisions on assumptions made during the high rate, high yield, increasing inflation regime of 2023Q3 – a regime it is increasingly evident we are no longer in.

Figure 2: Analyst Sentiment factors largely struggled in December; further evidence of a regime shift as the assumptions made by sell-side analysts no longer adequately explained the market environment

(Returns November 21 - December 20)

Source: Wolfe Research

GLOSSARY:

Beta: Measure of the volatility, or systematic risk, of a security or portfolio compared to the market as a whole (usually the S&P 500).

Register for Simplify's Investor Hub

In-depth case studies provide valuable insights into practical portfolio problems and their solutions

Simplify curated model portfolios that show investors how to incorporate alternatives into their portfolio

Stay up-to-date with our latest thoughts on markets via our weekly market commentaries