Measures of economic strength continue to surprise to the upside to start 2024, as does inflation. The first estimate of 2023Q4 GDP came in at 3.3%, beating the consensus estimate of 2% by 65%. The February non-farm payroll estimates came in at 353,000 – nearly double the consensus estimate (the January estimate was revised upward by 117,000 as well) – and the unemployment rate surprised by remaining at 3.7%. At the same time, the February estimate of inflation surprised to the upside at 3.1%, outpacing the consensus estimate of 2.9%.

All of this has combined to rattle interest rate futures markets, which had started the year predicting six rate cuts in 2024 – double what the Fed “dot plots” had predicted. If we continue to see upside surprises to key economic indicators, we will continue to see the first Fed rate cut – now slated for June – pushed into 2024H2. However, reprieve from inflation could be on the horizon. Shipping costs have decreased for four straight weeks, and the housing component of inflation, which lags other components of the consumer price index, is expected to continue to fall in the coming months despite an uptick in mortgage rates.

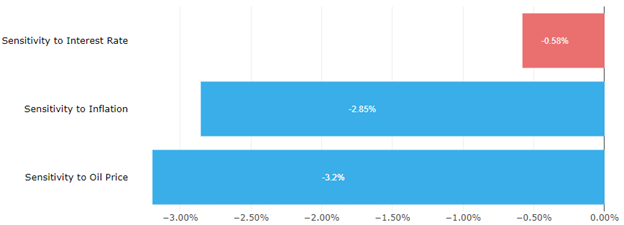

Both Value and Growth type factors showed mixed results in February, as the dynamically evolving interest rate landscape makes the Value vs. Growth trade difficult to determine. In terms of Growth, factors based on FQ1 and FY1 growth were more likely to see positive returns relative to factors based on FY2 or longer ranges. From Value’s perspective, Price-to-Sales factors performed well, while Free Cash Flow factors had strongly negative returns. For the second straight month Momentum factors gained, while Reversal lost as winners at the end of 2023 continued their winning streak further into 2024. Macro factors universally lost in February as oil prices remained largely flat, inflation continued to slow, and the market debate on when rate cuts will begin raged on (see Figure 1).

Figure 1: Macro Sensitivity Factors Universally Lost in February

(Returns January 23 – February 23)Source: Wolfe Research

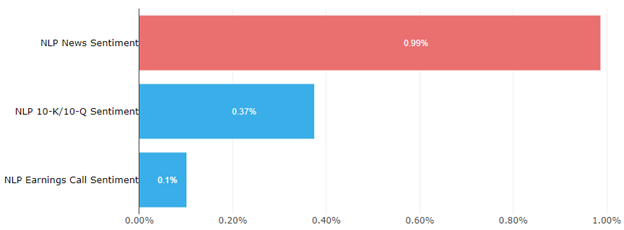

Conversely, NLP factors universally won in February, as the sentiment conveyed in news headlines, 10-K and 10-Q reports, and earnings calls successfully translated into stock performance (see Figure 2). Although not universal, Analyst Sentiment factors also performed well in the last month as the sell-side continued to correctly pick winners; EPS and Cash Flow Revision performed the best, while Recommendation Revision struggled.

Figure 2: NLP Factors Universally Won in February

(Returns January 23 – February 23)

Source: Wolfe Research

Turning to managed futures, the macro backdrop has created a pro-trend price action across many different markets, leading to exceptional recent performance in managed futures strategies. Surprisingly strong macro data in the US, alongside strong earnings reporting from the tech sector, all coupled with a slight increase in inflation measures, has catalyzed a major re-rating of the market’s expectations for the Fed’s interest rate pathway.

The consequent selloff in fixed income assets of all maturities has been in line with ongoing bearish trend indicators, contributing to futures trading returns. Meanwhile carry traders in bond markets have likely also done well in the selloff, as the inverted yield curve has indicated toward holding cash against short positions across both short-term interest rates and bond instruments. Looking ahead, the still inverted curve may continue to add a confirmatory signal to bearish short-term trend indicators, and it is our opinion many managed futures players will remain short global fixed income for now.

In the commodities sector, a powerful downtrend in the grains markets, which has been gathering momentum since last summer, gained additional momentum over February, further boosting returns. Meanwhile, energy and metals price action remained largely sideways, with a large countertrend reversal higher in natural gas catching some players offsides and forcing some short covering.

The standout market across all commodities, however, has been Cocoa. Supply-side concerns arising from weather, crop disease, and looming European deforestation regulations have caused the market to hit an all-time high amidst a 55% rally so far this year. The price action has been an explosive illustration of the blow-off tops that can occur in commodity markets once demand meets inelastic supply after stockpiles are mostly depleted. GLOSSARY:

Managed Futures: An investment where a portfolio of futures contracts is actively managed by professionals. Managed futures are considered an alternative investment and are often used by funds and institutional investors to provide both portfolio and market diversification.

Reversal: A change in the price direction of an asset. A reversal can occur to the upside or downside.

Register for Simplify's Investor Hub

In-depth case studies provide valuable insights into practical portfolio problems and their solutions

Simplify curated model portfolios that show investors how to incorporate alternatives into their portfolio

Stay up-to-date with our latest thoughts on markets via our weekly market commentaries