The Fed continues to showcase relatively dovish sentiment, even as both the economy and inflation remain stronger than expected. While futures markets were trending towards pricing in only two rate cuts in 2024, the Fed reinforced its expectation for three rate cuts this year at its March FOMC meeting. Against this backdrop stocks continue to reach new heights, most recently the S&P 500 and NASDAQ both set new records on March 21st. Despite this, macro risks remain. Inflation has missed to the upside two months in a row. Crude oil prices are pushing energy costs up, and the energy component of the CPI is transitioning from falling on a year-over-year basis to increasing on a year-over-year basis. This, coupled with the stubbornly slow pace with which the services less energy services component, which makes up 61% of the CPI by weight, is decreasing risks of further upward inflationary pressure. Expectations for NFP and GDP growth remain strong, continuing to give the Fed leeway in how it approaches its upcoming rate-cutting schedule.

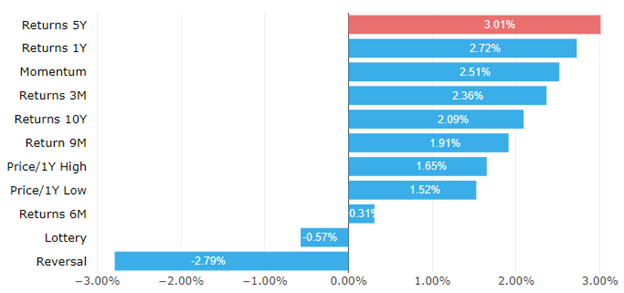

Macro sensitivity led factor gains this month, the largest of which was Sensitivity to Oil Prices as crude oil increased 5.3% over the past four weeks. Growth and Value continue to see mixed results as investors remain in limbo, unwilling to place large bets while waiting for a clearer indication of when rate cuts will begin. This same limbo was a boon to momentum-type factors (Figure 1). With no clear regime shift, momentum performed well in March, while Reversal struggled. Momentum was led by longer-horizon returns – 5Y Returns had the highest returns in the momentum category, followed by 1Y Returns. Quant factors were also mixed, with medium frequency quant increasing, while both low and high frequency quant falling. Not surprisingly, defensive quant also fell slightly as stocks overall were bullish in March. Overall March was a muted month for factor returns. In sigma terms, the largest movement came from Interim Cash Flow Growth (a growth factor) which increased only 1.48 standard deviations.

Figure 1: Momentum Benefits from the Value vs. Growth Limbo

(Returns Feb 23 - Mar 25)Source: Wolfe Research

March 2024 has been another strong month for managed futures, with industry tracking indices showing strong performance as trends continued to extend after February’s truly extraordinary run. In a notable divergence vs. recent months, long-term trend shorts in interest rate markets (both STIRs and bond futures) have generally not performed this month as US interest rates were caught in a range with relatively little impact from the ongoing data releases and March’s Fed meeting. International rate markets, meanwhile, experienced a mild counter-trend rally as some central banks seem to be taking the recent further clarification of the Fed’s pathway as the “all clear” to begin a mild sequence of cuts, with the Swiss National Bank moving first, and interest rate expectations also being revised lower in the UK and EU.

However, other markets fared far better for managed future strategies in March. Firstly, in Equities, long positions have performed well as 2024’s ongoing rally continues to extend in line with bullish trend, carry, and cross-asset relative value signals. The relatively low volatility conditions that have prevailed during this move, we believe have allowed traders to position strongly and capitalize on it.

In FX, the USD’s reasonably sideways price action in line with tepid US interest rate markets has benefitted cross currency carry trades, whilst the ongoing upside trend extensions in Crypto on the back of continued ETF flows are also likely to have benefitted some managers.

But the greatest excitement this month has surely been in commodity markets. First, there was the remarkable extension in Cocoa prices, fuelled by a full-on supply shortage, which has fuelled very strong returns to trend following, driving returns for many managers YTD in 2024. The shortage, driven by poor weather, crop disease, and previous years' depletion of inventories, is now at an acute phase and causing disruptions to downstream processors, which may be the only way to curtail final endpoint demand. Returns in the rest of softs and agricultural markets have appeared more measured, with all eyes on Cocoa.

In the Energy sector, natural gas continues to trade with a bearish tilt, in line with still bearish trend indicators. Meanwhile, oil markets have notably diverged higher on continuing risks of geopolitical supply disruption and the perception that 2023’s US oil production growth theme may now slow, in response to cost efficiency pushes, producer M&A, and other factors. Bullish trend and breakout signals in oil have largely performed as a result.

Metals markets have also been attracting more attention, with gold making new all-time highs in line with breakout indicators, but failing to sustainably trend through time. These new highs have happened despite ongoing outflows from ETFs and high US interest rates. Market participants are currently debating whether this notable and episodic relative value divergence is an early warning sign re: US fiscal imbalances or whether it instead represents evidence of a growing shift of central bank portfolio compositions, or both. For now, the relative stability in market pricing of US inflation expectations seems to argue more for the overseas rebalancing argument. Finally, copper and other base metals continue to trade in a range, with market participants keenly watching to see if a sustained copper breakout is possible given ongoing supply constraints.

GLOSSARY:

Managed Futures: An investment where a portfolio of futures contracts is actively managed by professionals. Managed futures are considered an alternative investment and are often used by funds and institutional investors to provide both portfolio and market diversification.

Reversal: A change in the price direction of an asset. A reversal can occur to the upside or downside.

Register for Simplify's Investor Hub

In-depth case studies provide valuable insights into practical portfolio problems and their solutions

Simplify curated model portfolios that show investors how to incorporate alternatives into their portfolio

Stay up-to-date with our latest thoughts on markets via our weekly market commentaries