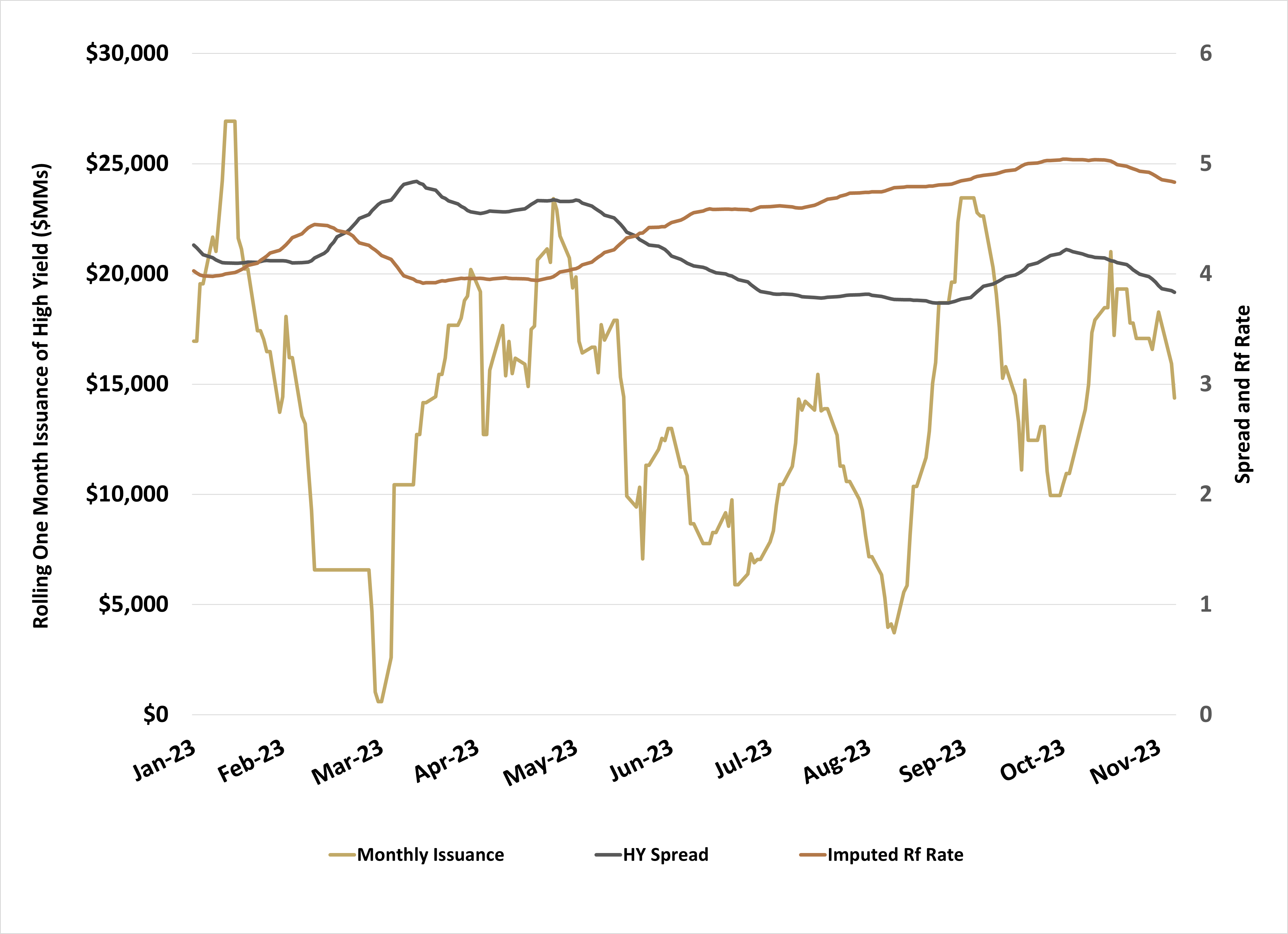

High yield credit spreads tightened alongside the risk-on environment in November, declining from a historically average 437 bps to a somewhat loose 374 bps. Issuance in high yield rose with the easing of financial conditions, but overall issuance has remained muted relative to lower interest rate environments, despite the shift from loans to fixed rate bonds.

Figure 1: High Yield Issuance Trailing One Month vs. Rates

Source: Simplify Asset Management, Bloomberg

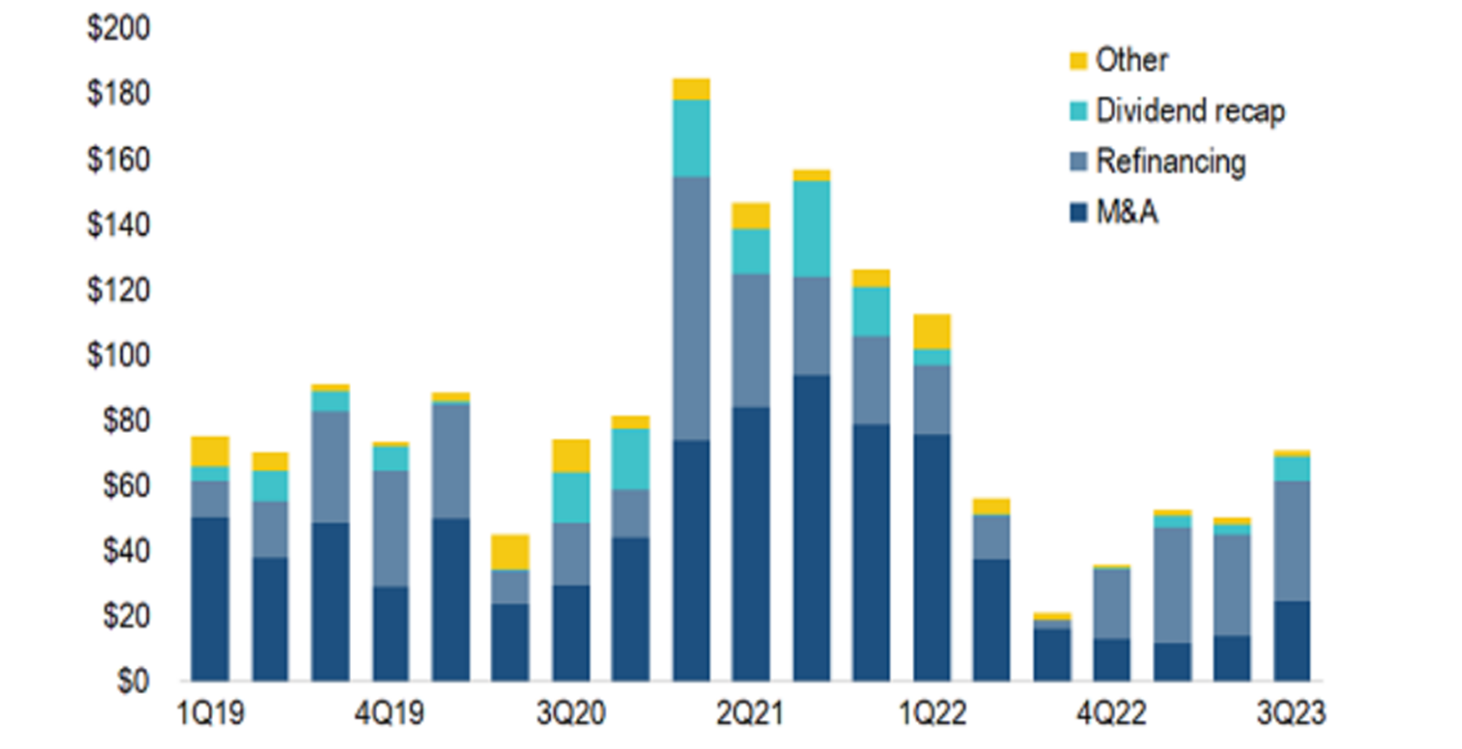

Figure 2: US Institutional Loan Volume ($B)

Source: PitchBook | LCD Data Through Sept 25, 2023

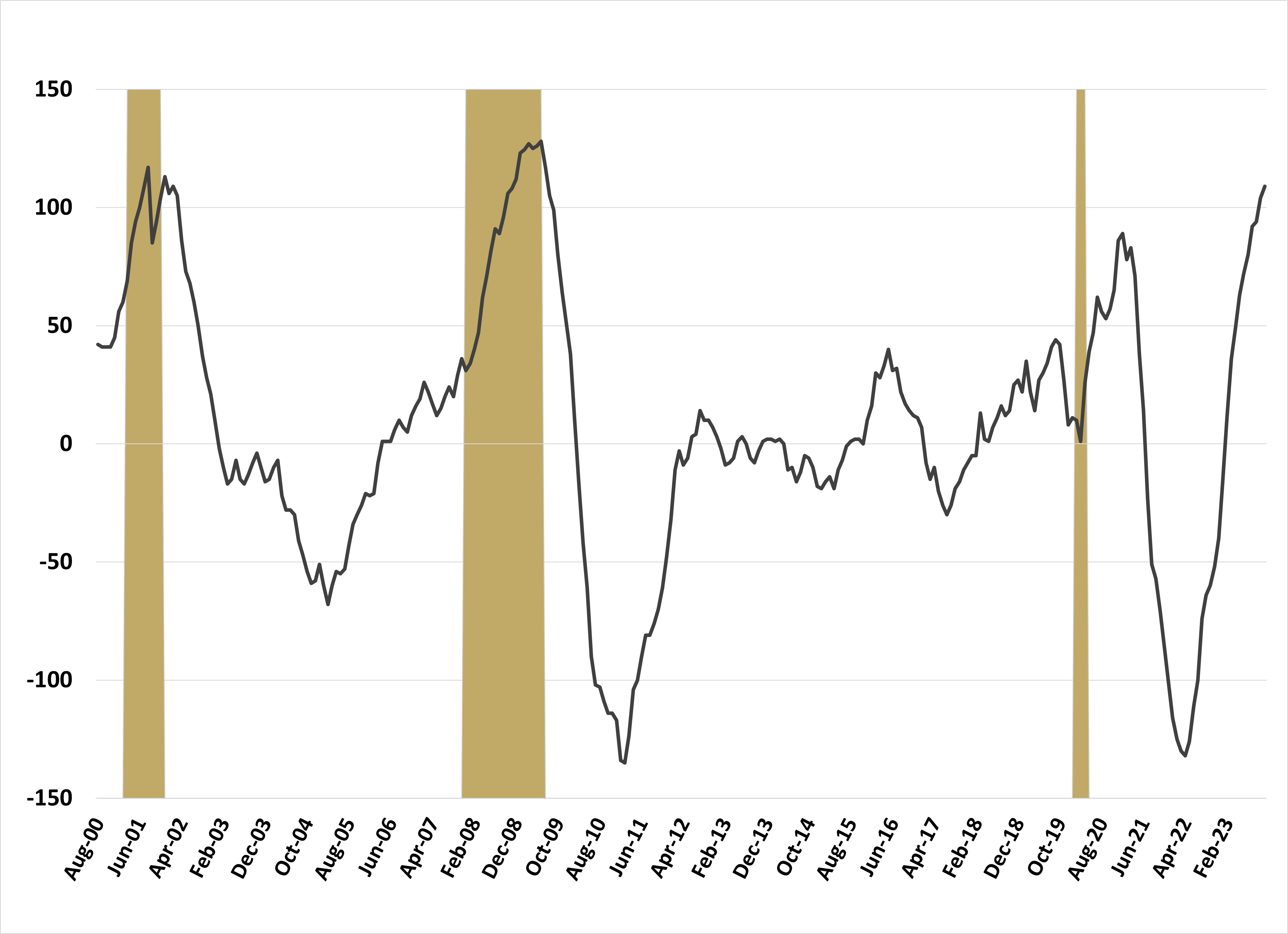

Our credit spread model also tightened, more than the index in fact. The primary driver was a mid-month improvement in the NY Fed’s Empire General Business Conditions, which returned to expansion. However, the model continues to suggest that high yield credit spreads sit at roughly half of warranted levels. Similar divergences have preceded major credit events and it’s worth noting that this type of increase in bankruptcies has always accompanied recessions. To see these levels without a recession would be surprising.

Figure 3: Trailing Twelve-Month Change in Bankruptcies

Source: Simplify Asset Management, Bloomberg

As we noted last month, the level of interest rates appeared to be the primary driver of this distress, leaving us surprised by the move higher in risk-free rates over the summer. We noted that there were two possible alternatives:

A buyer’s strike driven by competing investment alternatives reducing demand for global risk-free bonds

An increase in bond issuance without a corresponding increase in demand, as marginal capital flows are not responding to the increased opportunity set due to various factors (linked to reason #1)

Rather than adopt a single-factor rationale, we continue to believe it’s a combination of the two as higher interest rates do not necessarily invoke comparison shopping between risk-free bonds, credit investments like high yield, and equities (or private alternatives) in the modern “fixed allocation” model portfolio world. While investors were slow to recognize the opportunity in risk-free bonds, we’ve begun to see reallocation; ironically, this rally in risk-free bonds provides increased buying power for other risk assets leading to an “everything rally.”

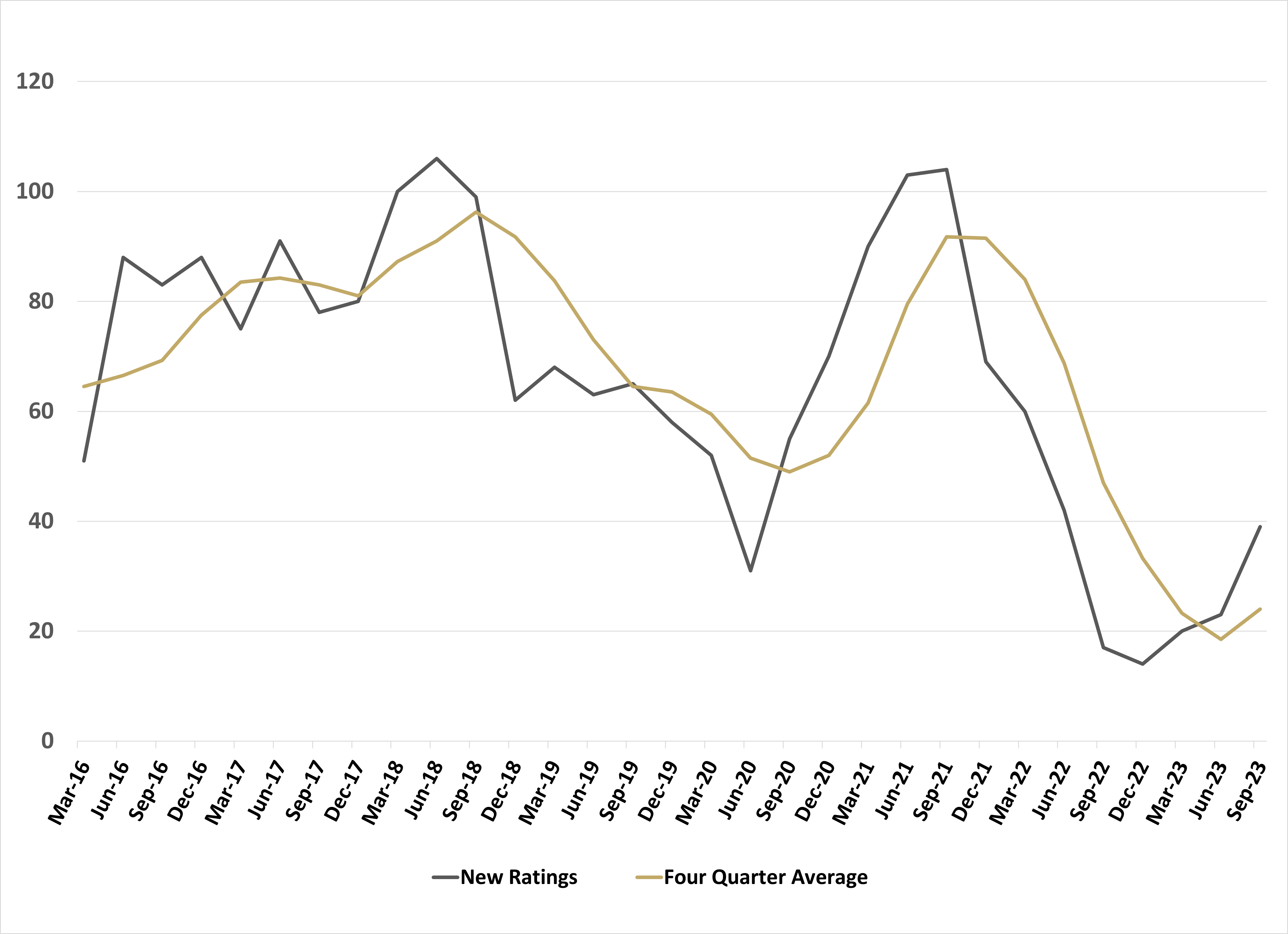

While the focus is increasingly on Fed rate cuts for 2024, the question remains whether it will come fast enough. The recent increase in issuance is helpful, but the average maturity for high yield bonds continues to fall and the 2024/2025 maturity wall threatens to move into “current liabilities” from an accounting standpoint. This would lead to increased risks of a credit downgrade cycle. With credit market issuance remaining in the doldrums, time is growing short.

Figure 4: New Issue Credit Ratings

Source: Simplify Asset Management, Bloomberg

GLOSSARY:

Basis Points: A common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%.

Register for Simplify's Investor Hub

In-depth case studies provide valuable insights into practical portfolio problems and their solutions

Simplify curated model portfolios that show investors how to incorporate alternatives into their portfolio

Stay up-to-date with our latest thoughts on markets via our weekly market commentaries