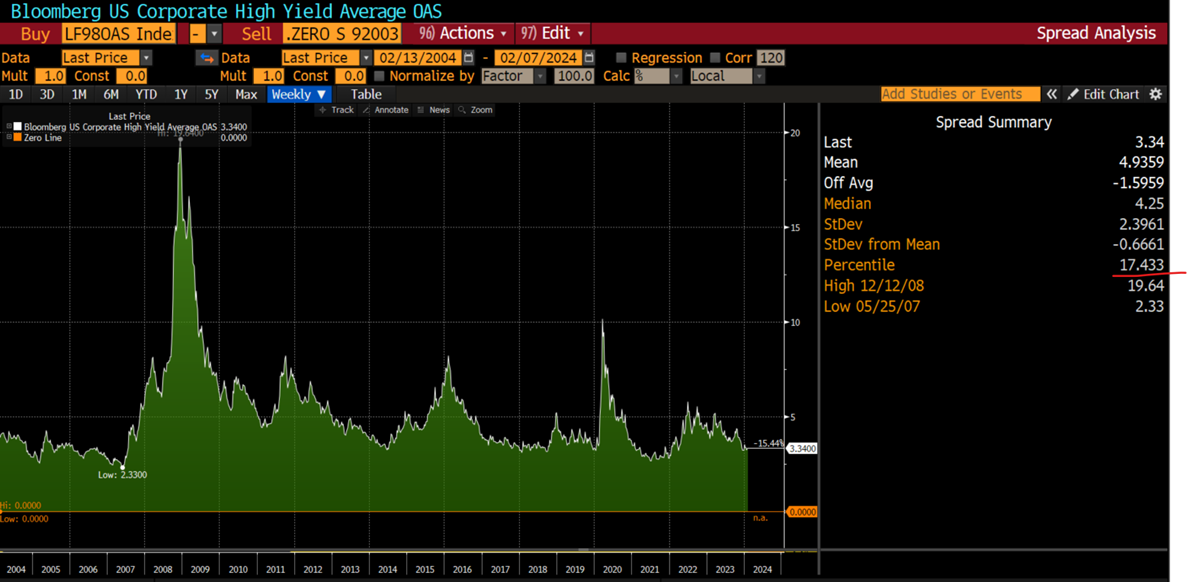

After the sharp rally in 4Q 2023, credit spreads appear to have stabilized near the cheapest quintile in history (see Figure 1). While our primary credit hedge continues to be our Quality-Junk overlay, which was designed specifically to rally during credit events, we are also using the recent tightness in CDS to begin diversifying our protection sources, introducing credit default swaps on the high yield index into our credit hedging books. With credit spreads still very tight versus history, we like our odds being aggressively hedged here.

Figure 1: High Yield Credit SpreadsSource: Bloomberg

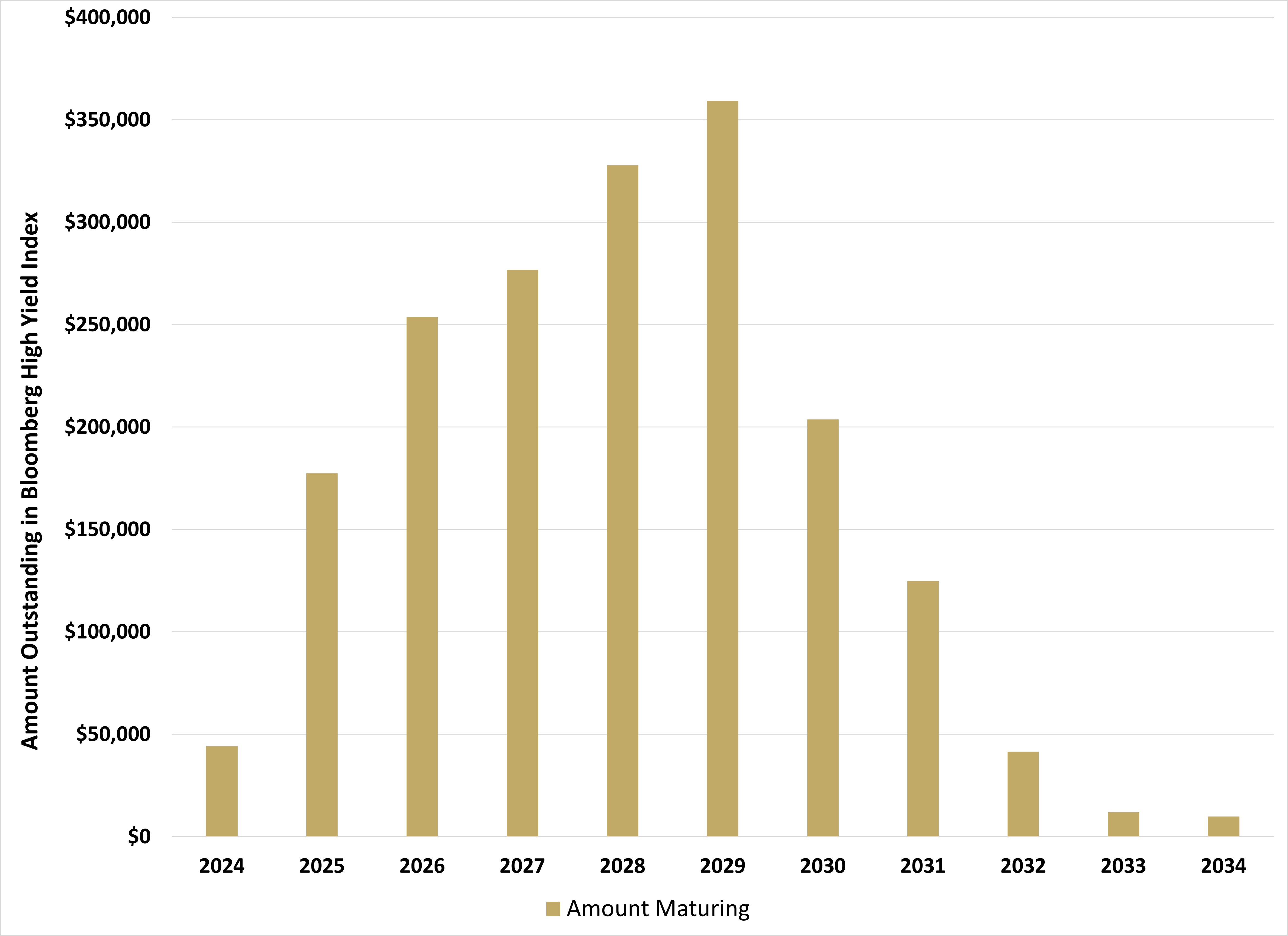

This is particularly true given the record refinancing wall that sits ahead of us (see Figure 2). For most high yield borrowers, it is imperative to not allow debt maturities to coast within one year of expiry, converting to “Current Liabilities” on their balance sheets. This means that the remaining maturities of 2024 and the maturities of 2025 are “must-do” business for this year.

Figure 2: High Yield Index Maturities Source: Bloomberg, Simplify Asset Management

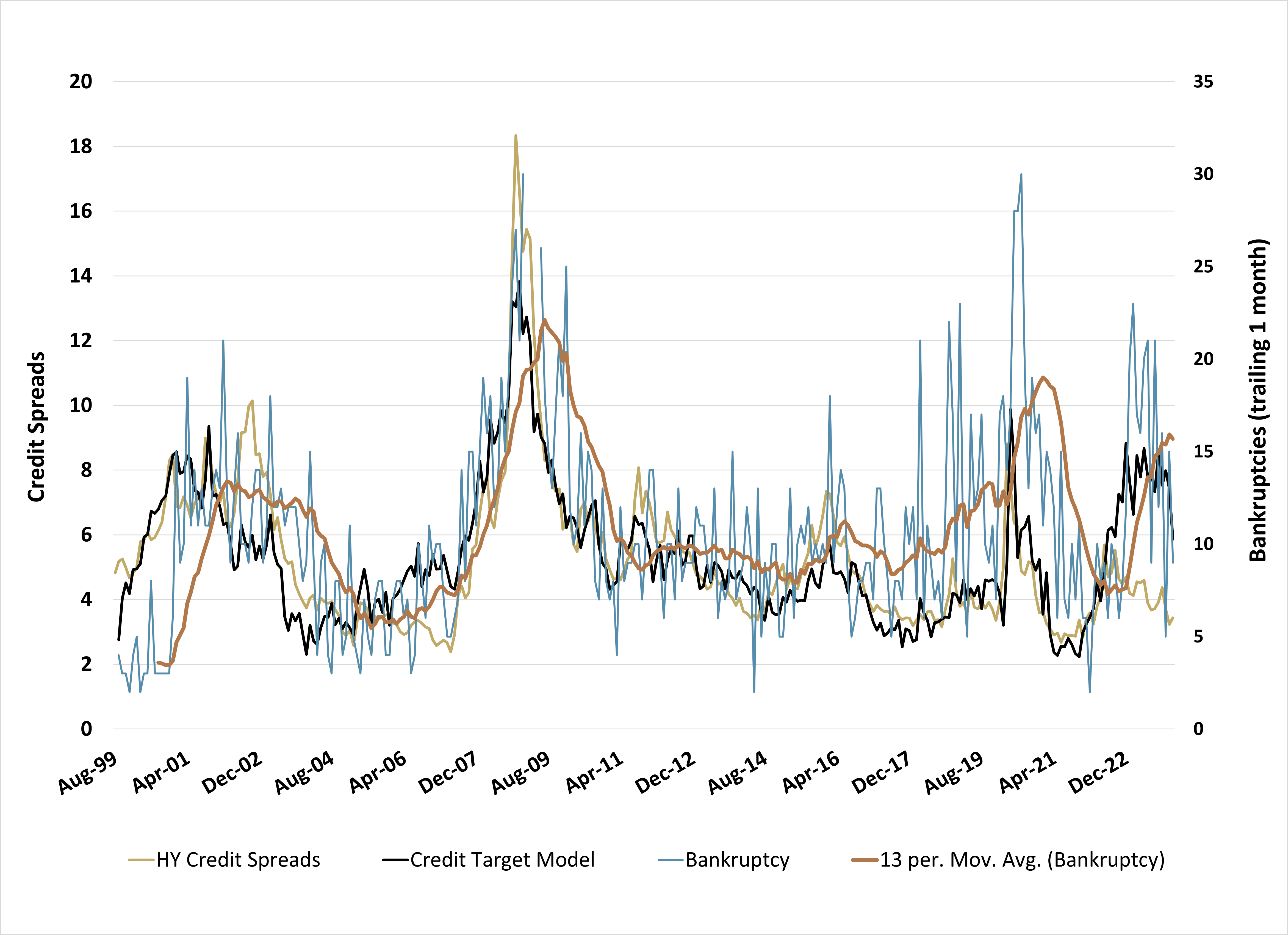

There has been a significant tightening of our credit spread model (see Figure 3), as new orders turned positive in both the ISM manufacturing and non-manufacturing indices, and Senior Loan Officer surveys remained unchanged. This is not uncommon in the first few months of a recession, as delayed orders finally work inventories down to levels that require a rebuild, and credit officers pause to see if the recent tightening of credit conditions slows charge-offs.

Providing some confirmation of this improvement, bankruptcies slowed in the first month of 2024, although it’s unclear if this is a seasonal dynamic. We should know in short order if the proverbial soft landing is here. If, on the other hand, deterioration reasserts as we expect, credit spreads should widen rapidly.

Figure 3: Credit Spread Model Source: Bloomberg, Simplify Asset Management

GLOSSARY:

Credit Default Swap (CDS): A financial derivative that allows an investor to swap or offset their credit risk with that of another investor.

Quality Minus Junk: The return of a basket of 100 stocks whose bond rating is investment grade minus the return of 100 stocks whose bond rating is below investment grade (junk).

Register for Simplify's Investor Hub

In-depth case studies provide valuable insights into practical portfolio problems and their solutions

Simplify curated model portfolios that show investors how to incorporate alternatives into their portfolio

Stay up-to-date with our latest thoughts on markets via our weekly market commentaries