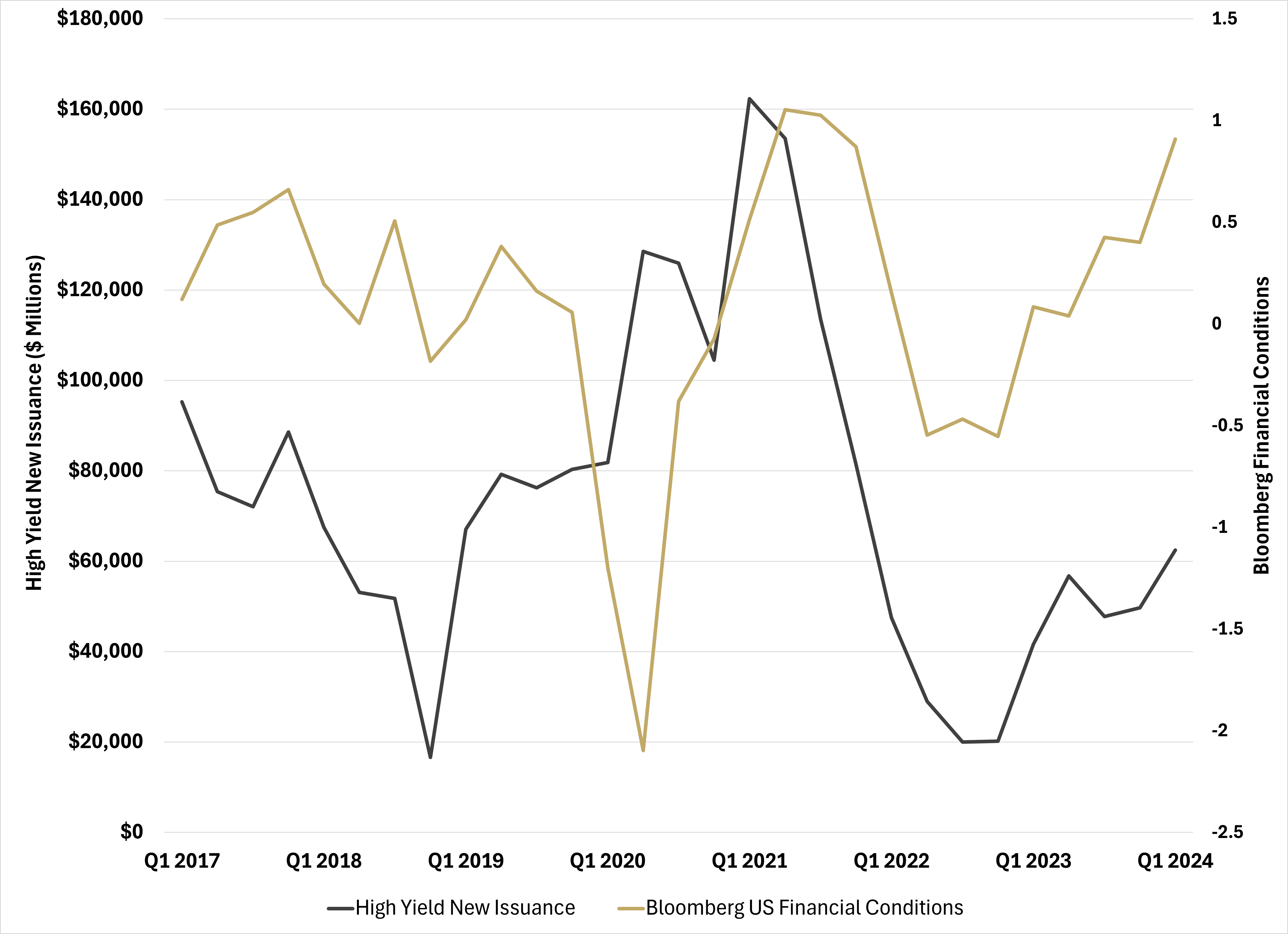

After a brief pause at the end of January, we have seen continued year-to-date tightening of credit spreads. We are currently sitting below the 15%ile in history (see Figure 1). Despite these tight credit spreads and perceived loose financial conditions, new issuance remains depressed at less than half the levels of 2020 (see Figure 2).

Figure 1: High Yield Credit SpreadsSource: Bloomberg

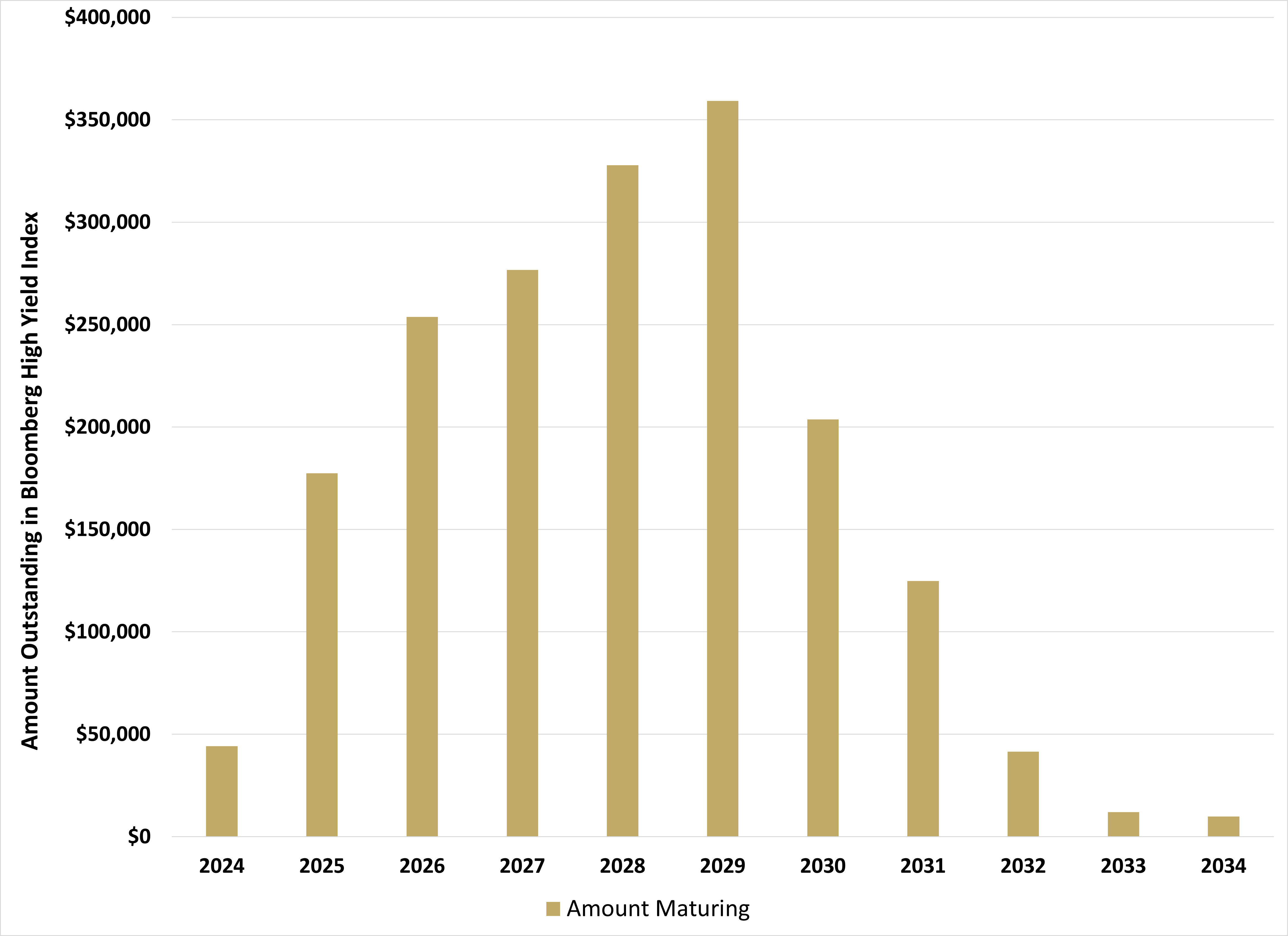

Given the looming maturity wall for high yield (see Figure 3), we continue to believe the tight credit spreads are a byproduct of the limited issuance. As coupons flow to credit managers, they can either build cash positions or reinvest the coupons into existing secondary issues. The evidence suggests they are doing the latter.

Figure 3: High Yield Index MaturitiesSource: Bloomberg, Simplify Asset Management

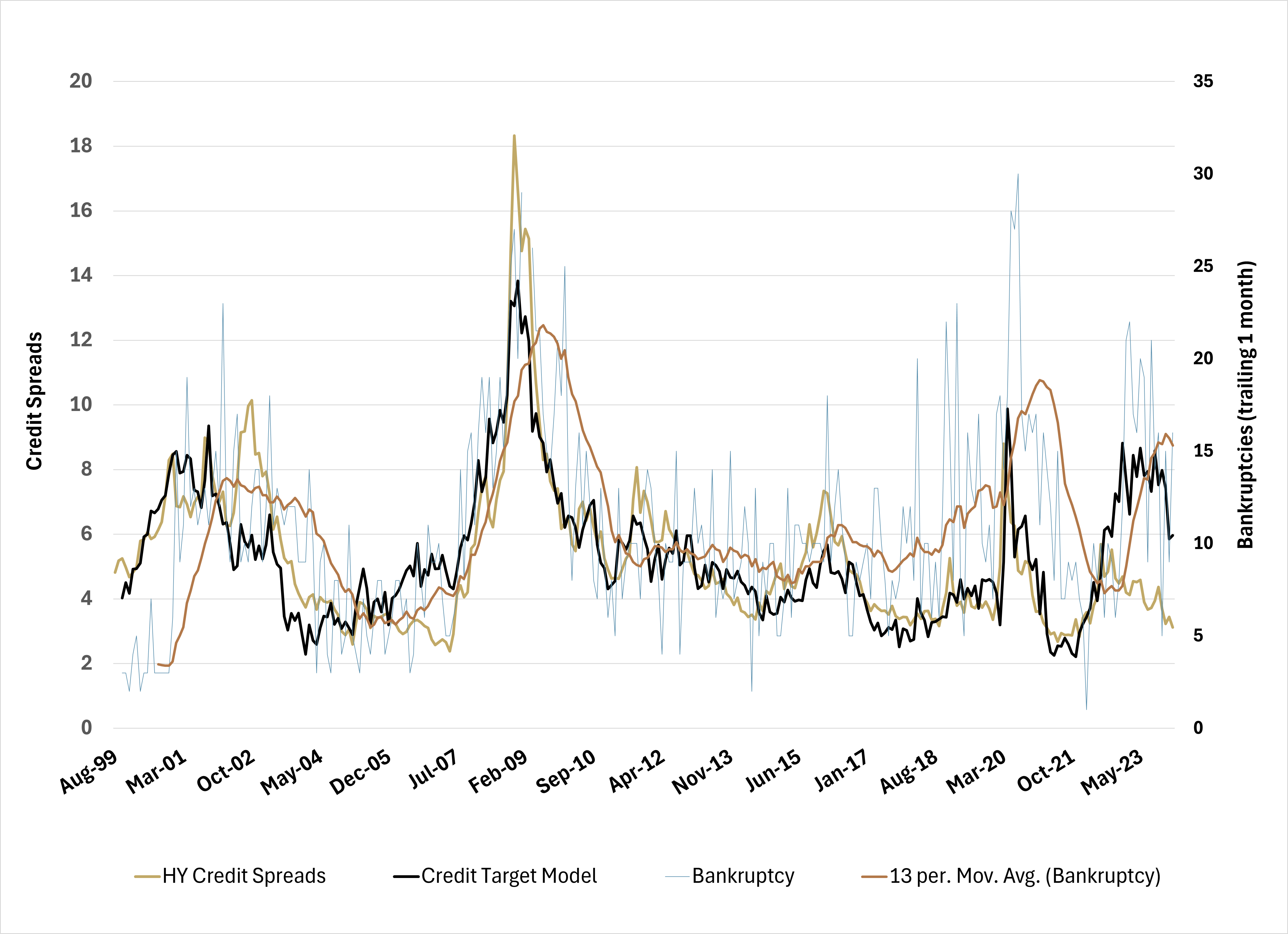

Similar dynamics in 2006/7 contributed to the unexpectedly tight credit spreads that existed directly ahead of the largest credit event of the last 50 years (see Figure 4).

The tightening of our credit spread model (see Figure 4) tied to improvements in the New Orders component of the ISM surveys has begun to reverse. As we noted last month, this behavior is not uncommon in the first few months of a recession, as delayed orders finally work inventories down to levels that require a rebuild, and credit officers pause to see if recent tightening of credit conditions slows charge-offs.

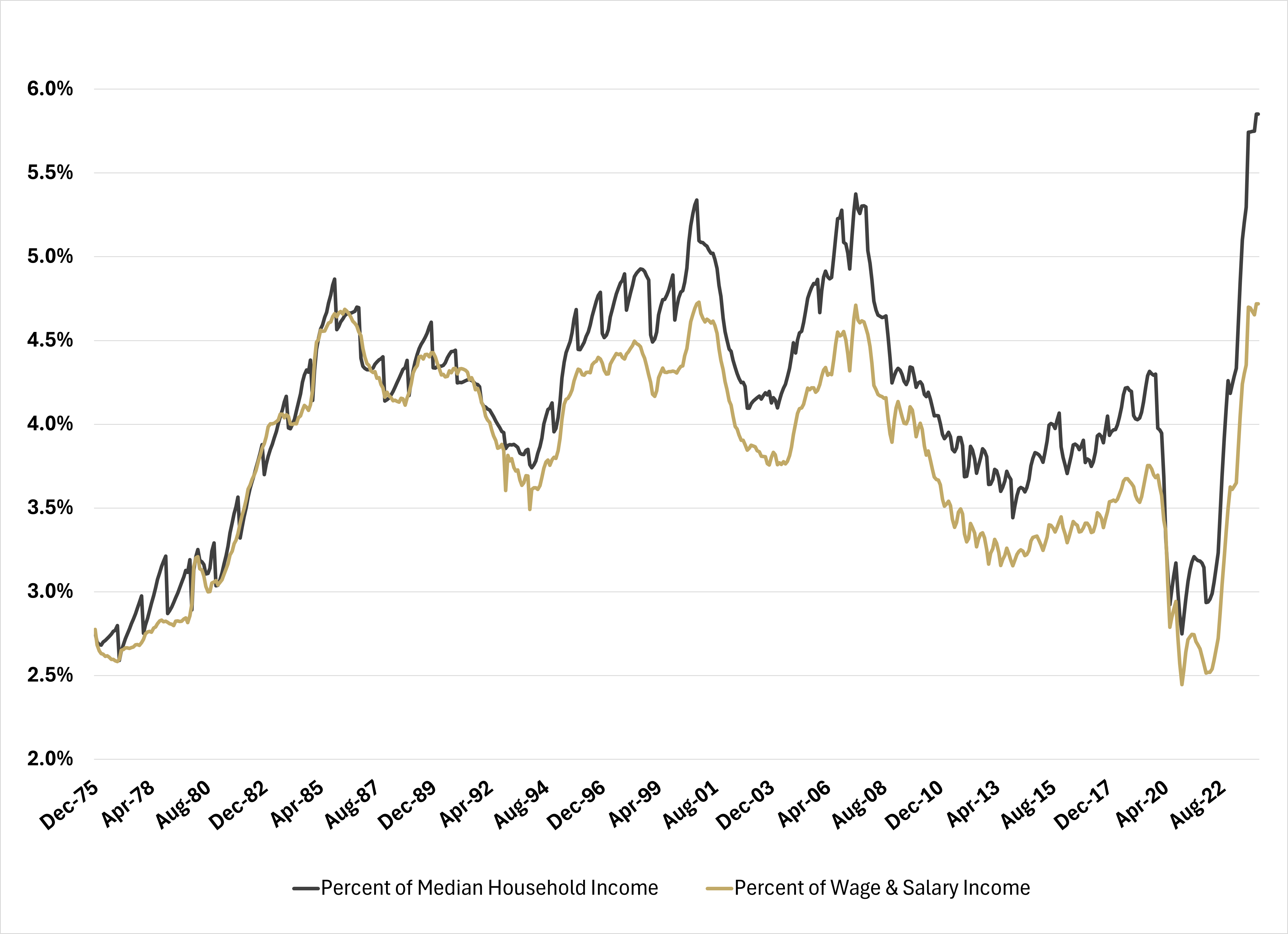

After a pause at the start of the year, bankruptcies have again rebounded, and charge-offs are accelerating in many areas of the economy as the levels of interest paid by households is now accelerating rapidly (see Figure 5). It remains to be seen if it is indeed different this time.

Figure 5: Personal Interest Expense as % of IncomeSource: BEA, Simplify Asset Management

Register for Simplify's Investor Hub

In-depth case studies provide valuable insights into practical portfolio problems and their solutions

Simplify curated model portfolios that show investors how to incorporate alternatives into their portfolio

Stay up-to-date with our latest thoughts on markets via our weekly market commentaries