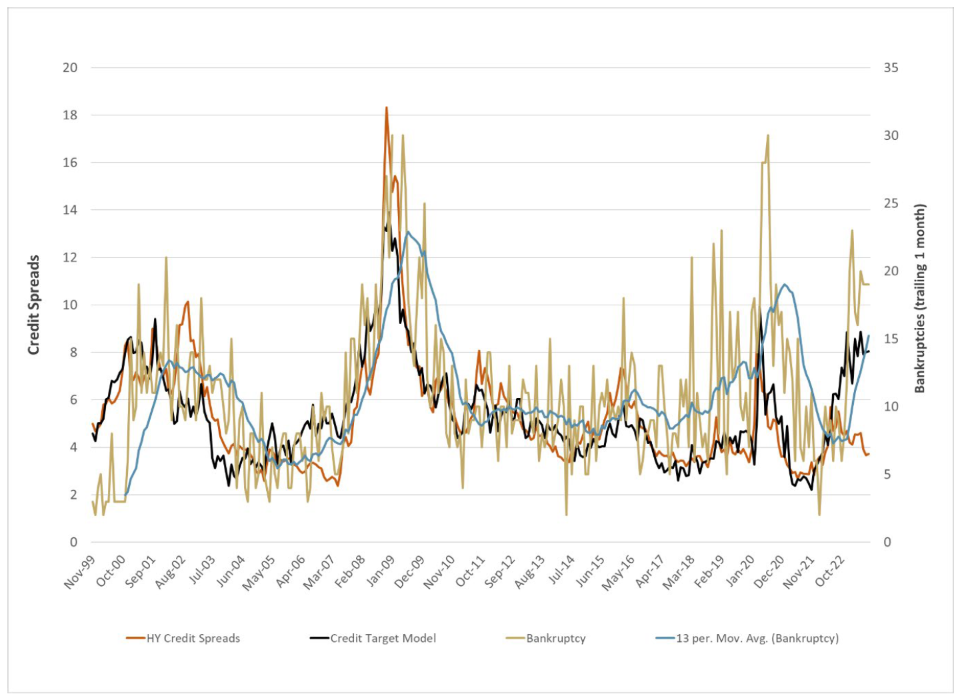

High yield credit markets continued to tighten despite deteriorating conditions in large corporate bankruptcies. Year-to-date in 2023, we’ve experienced 148 corporate bankruptcies with assets greater than $50MM in assets, more than double the pace from 2022 (60), and even more than the first eight months of 2008 (132). Our credit spread model (Figure 1) continues to suggest that high yield credit spreads sit at less than half of warranted levels. Unfortunately, this model appears quite consistent with realized bankruptcies and realized spreads historically.

Similar but much smaller divergences appeared in late 2019 and early 2007, and ultimately resolved with much higher credit spreads as corporate profits plummeted due to recessionary conditions. The immediate and unprecedented stimulus of 2020 ended that most recent credit cycle unresolved, while the delays associated with the 2008 crisis ultimately led to credit spreads moving to near-record levels. Unfortunately, the diminished appetite for further stimulus and fears of inflation returning suggest our current episode has much more in common with 2008 than 2020.

There are three key factors influencing the tighter-than-expected credit spreads in our analysis:

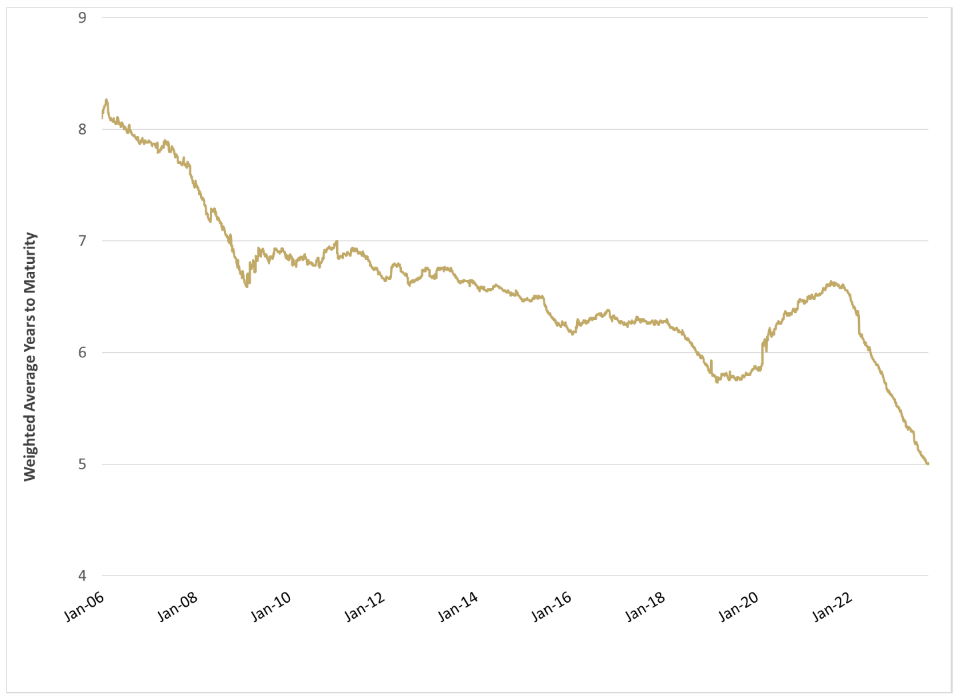

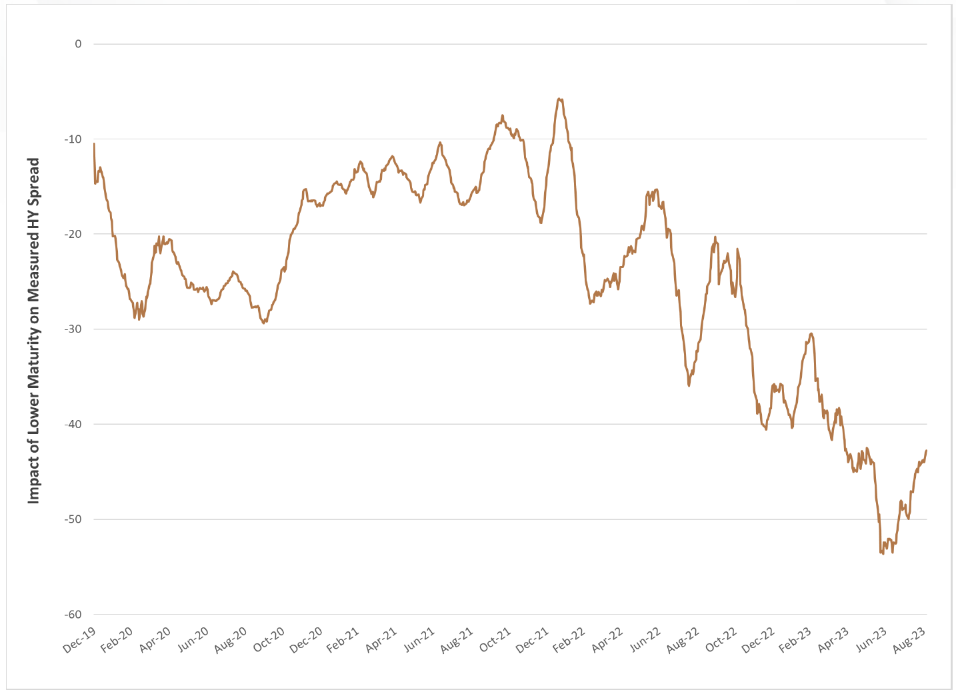

1.The higher levels of interest rates have led to a collapse in high yield issuance and an unprecedented decline in the weighted average maturity of the high yield index (Figure 2). Going into 2008, the average maturity of the high yield index sat near 7.5 years. Today, the index has plummeted to record lows at 5 years. Our models suggest this shortening of duration against an inverted yield curve has “artificially” tightened spreads by roughly 40 bps (Figure 3).

Figure 2: Bloomberg High Yield Index Years to MaturitySource: Simplify Asset Management, Bloomberg

Figure 3: Impact of Maturity on HY SpreadSource: Simplify Asset Management, Bloomberg

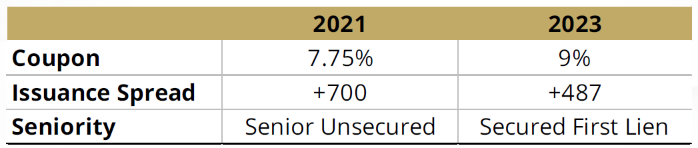

2.The limited issuance that has occurred has meaningfully improved the position of creditors through increased seniority in the capital stack and a material increase in coupon. These reduce risks for new lenders even as the newly issued paper has degraded the claims of prior lenders and likely significantly reduced the long-term viability of the company. A good example is a recent issue by Clear Channel Outdoor, a highly levered billboard advertising roll-up that has struggled since going public in 2005. Comparing the experience of the company in issuing bonds in 2021 versus 2023 is instructive (Figure 4).