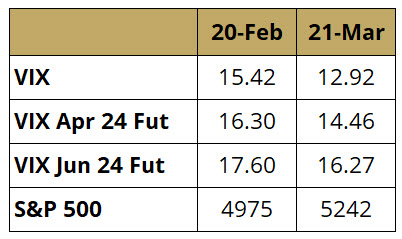

VIX has declined since our last update alongside the strong rally in equities, keeping the level of VIX significantly below historical averages. Low VIX, however, generally results in a very steep (contango) VIX futures curve, and futures slide down to create a very positive roll yield when shorting VIX, as we can see for two representative parts of the curve in Table 1.

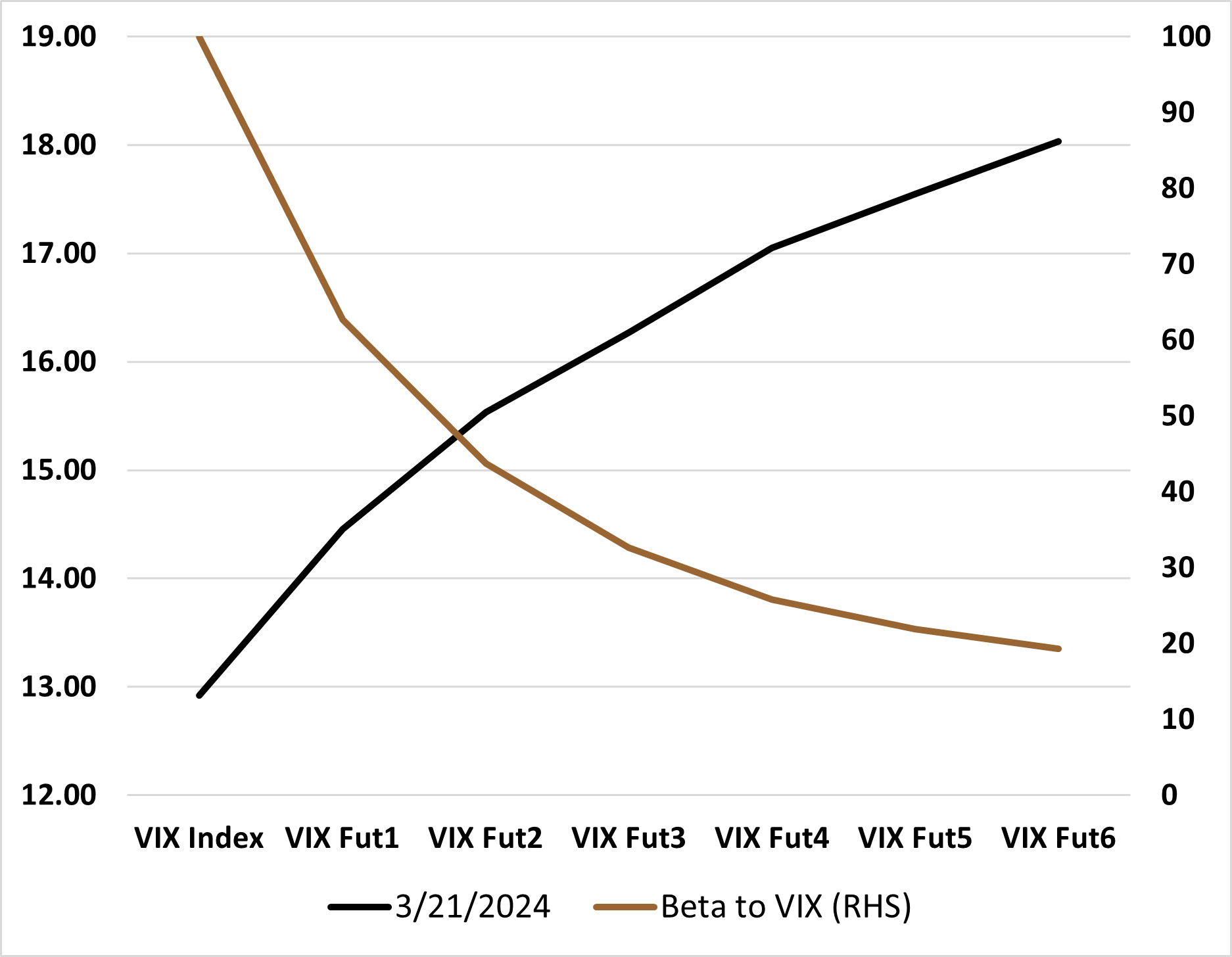

The VIX curve has the potential to remain steep as election-related uncertainties may keep the long dated VIX curve elevated. Also notable is that while roll down may be highest in the very front contracts, so is the risk. Figure 1 shows that long-dated VIX contracts have significantly lower beta to VIX, with albeit a much lower roll down. The optimal risk-reward tradeoff between beta and roll yield indicates the optimal point continues to be near the third VIX contract.

Figure 1: VIX Term Structure vs. Beta to VIXSource: Bloomberg, Simplify Asset Management

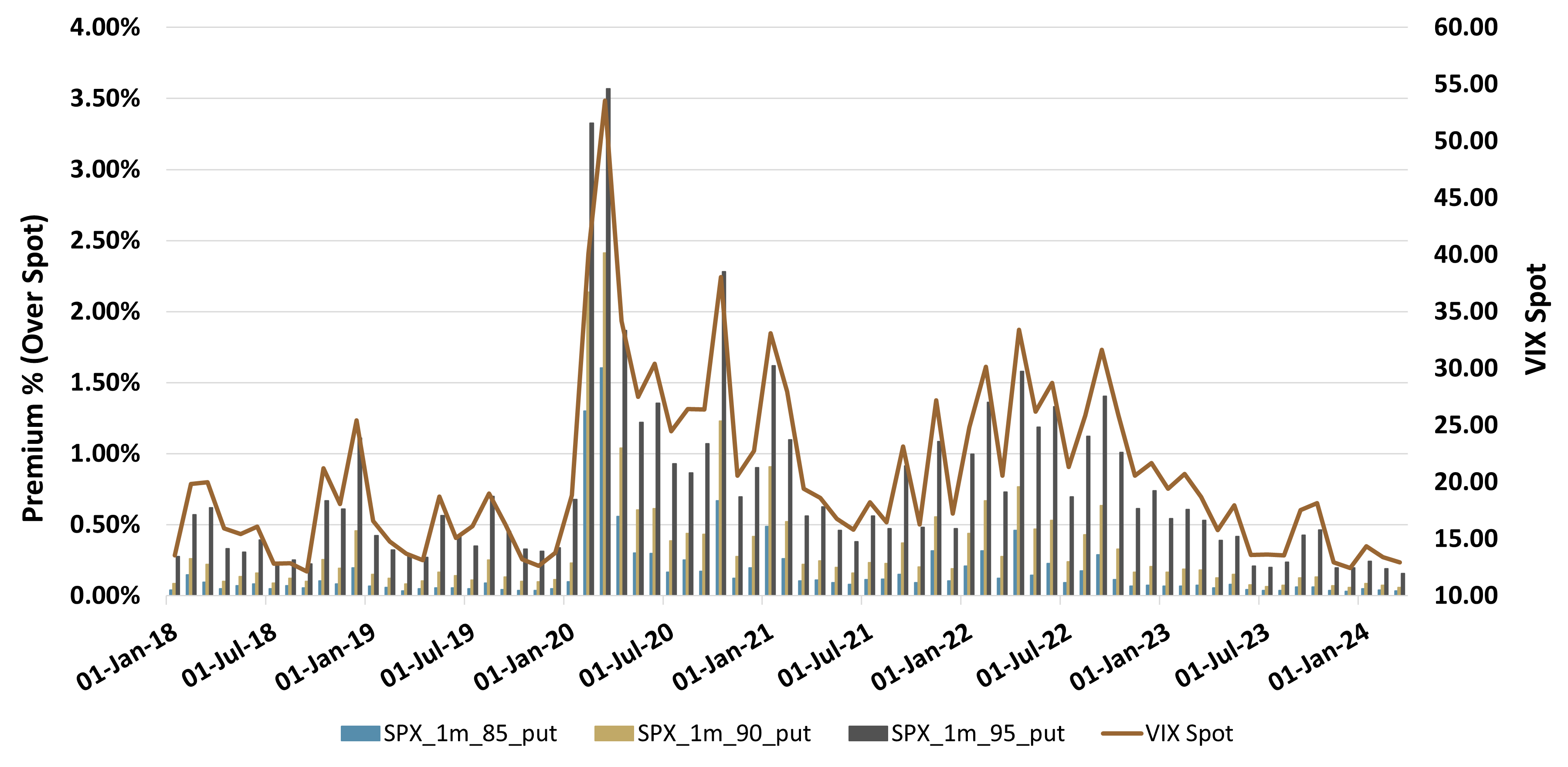

With VIX’s continued moving lower over the last month, SPX OTM put premia were pushed to their lowest levels since 2018, creating the cheapest 1-month 5% out-of-the-money downside protection of the last six years (see Figure 2).

Figure 2: Cost of 1-Month SPX Put Protection at

100% Notional (LHS) vs. VIX (RHS)

Source: Bloomberg, Simplify Asset Management

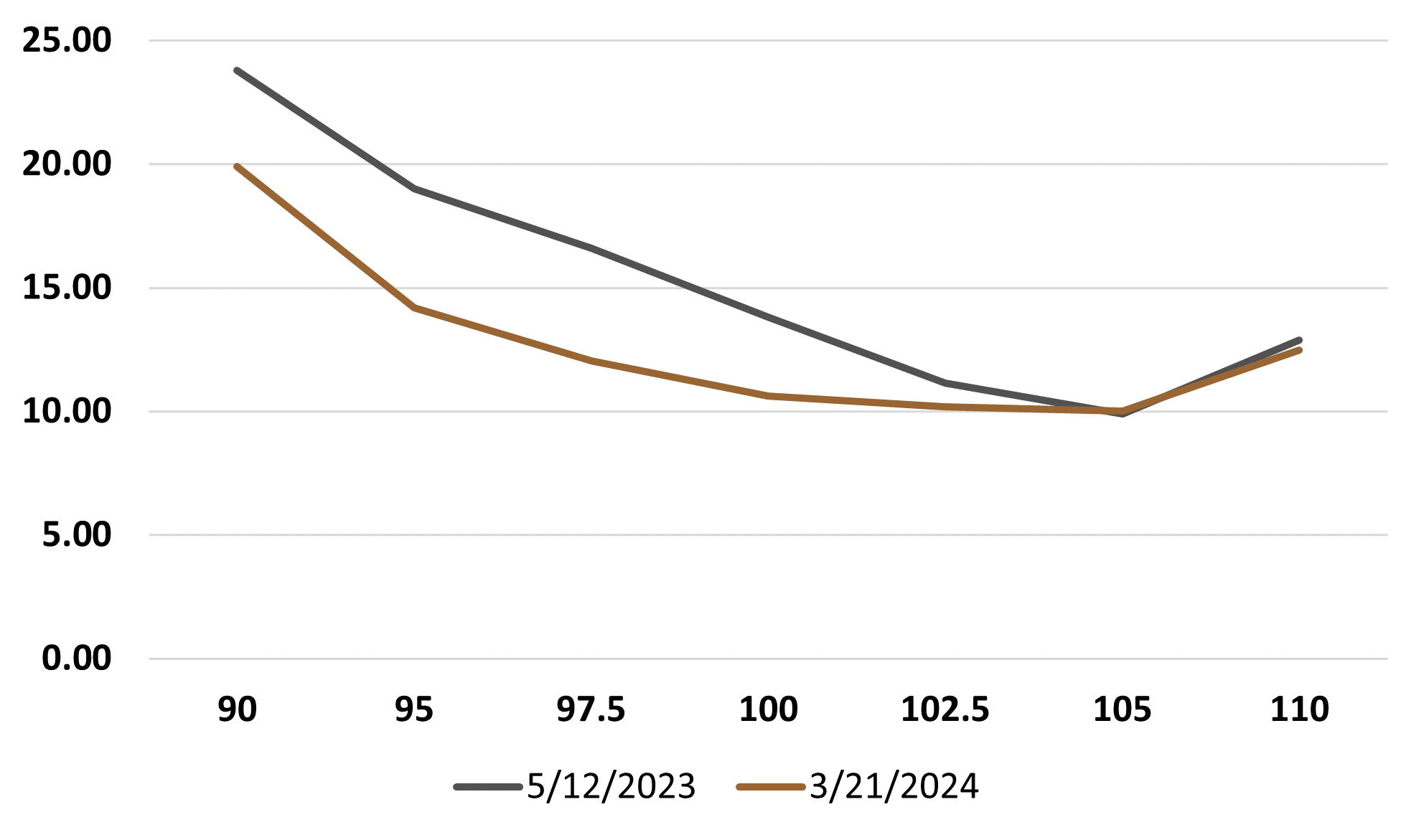

In our December update, we discussed the flattening of the volatility curve since May last year (Figure 3), and how that might be creating opportunities for the implementation of “zero-cost” collar hedging strategies (i.e. long stock, long protective put spread, short call to fully fund the puts) since out-of-the-money calls would become closer in price to their put counterparts, placing the upside cap at a higher level.

Figure 3: Vol Skew for 1-Month SPX Options – May 2023 vs. Mar 2024Source: Bloomberg, Simplify Asset Management

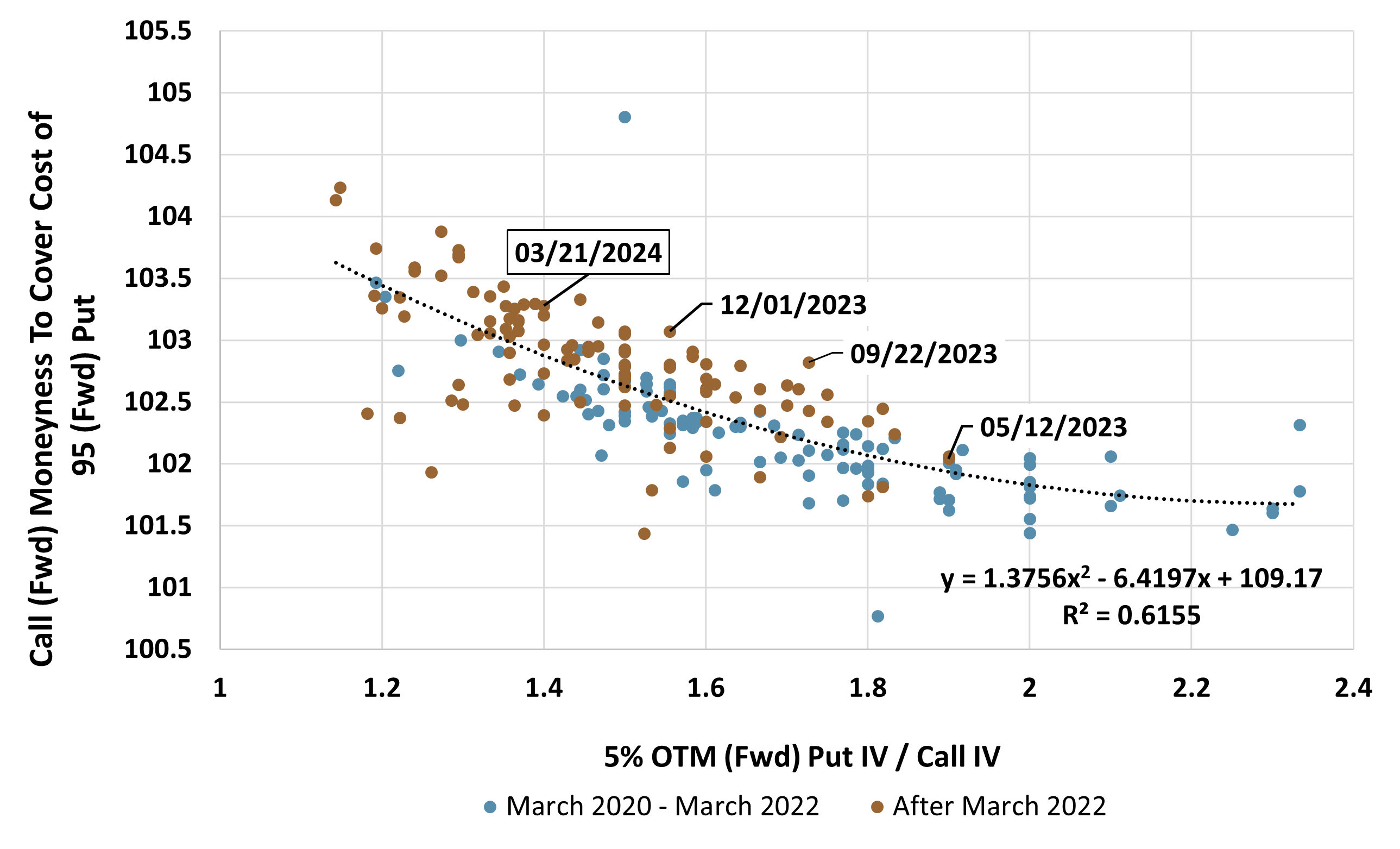

Figure 4 below shows the relationship between vol skew (5% OTM Put IV / Call IV) and the call moneyness required to fund a 95 moneyness put, alongside the overall impact of the interest rates hike after March 2022 (another important factor for costless collar strategies making calls synthetically more expensive). As we can see, between May 2023 and March 2024, the vol skew has come down from 1.9 to 1.4 levels, allowing for an extra 1% upside from the short call.

Figure 4: Impact of Volatility Skew and Interest Rates on Put-Call Relative PricingSource: Bloomberg, Simplify Asset Management

Glossary:

Contango: A situation where the futures price of an asset is higher than the spot price. This results in an upward-sloping forward curve.

Option: An option is a contract that gives the buyer the right to either buy (in the case of a call option) or sell (in the case of a put option) an underlying asset at a pre-determined price ("strike") by a specific date ("expiry"). An "outright" is another name for a single option leg. A "spread" is when options are bought at one strike and an equal amount of options are sold at a different strike, all at the same expiry.

VIX Index: A real-time market index representing the market's expectations for volatility over the coming 30 days.

Register for Simplify's Investor Hub

In-depth case studies provide valuable insights into practical portfolio problems and their solutions

Simplify curated model portfolios that show investors how to incorporate alternatives into their portfolio

Stay up-to-date with our latest thoughts on markets via our weekly market commentaries