Share

Diversification is Easier in Theory Than in Practice

Talking to clients about portfolio diversification is easy. We all know the script: "We might need to add some uncorrelated investments that can help protect you when stocks tank." To make room for the alternatives you move a client from, say, a 60/40 stock/bond allocation to 50/30/20.

Things may go well for a while. The hard part comes when alternatives underperform for a year or two. The client starts questioning the allocation. The behavioral friction builds.

The script for when stocks decline is well known: “Hey, the market is down. We just need to hold and not get scared out of the market so we can potentially benefit from the rebound.” But when stocks are up, and the alternative investment is not, the conversation might become: “Tell me again why you bought that thing.” It's tough to stay disciplined when you're justifying the underperforming slice of the portfolio, especially when it’s out of the benchmark.

Here’s a Potential Solution – Clients Can Have Their Cake and Eat It Too

Capital efficient strategies are a potential solution. They’ve been around for a long time. Sometimes they’re called return-stacking. Others call them portable alpha. The concept is to add an alternative, non-correlated asset on top of the core equity or bond position, not instead of it.

Simplify has recently introduced a capital efficient strategy – the Simplify US Equity PLUS Managed Futures Strategy ETF (CTAP).

CTAP combines 100% exposure to U.S. large-cap stocks PLUS 100% exposure to managed futures – a strategy that has historically provided a source of non-correlated returns.

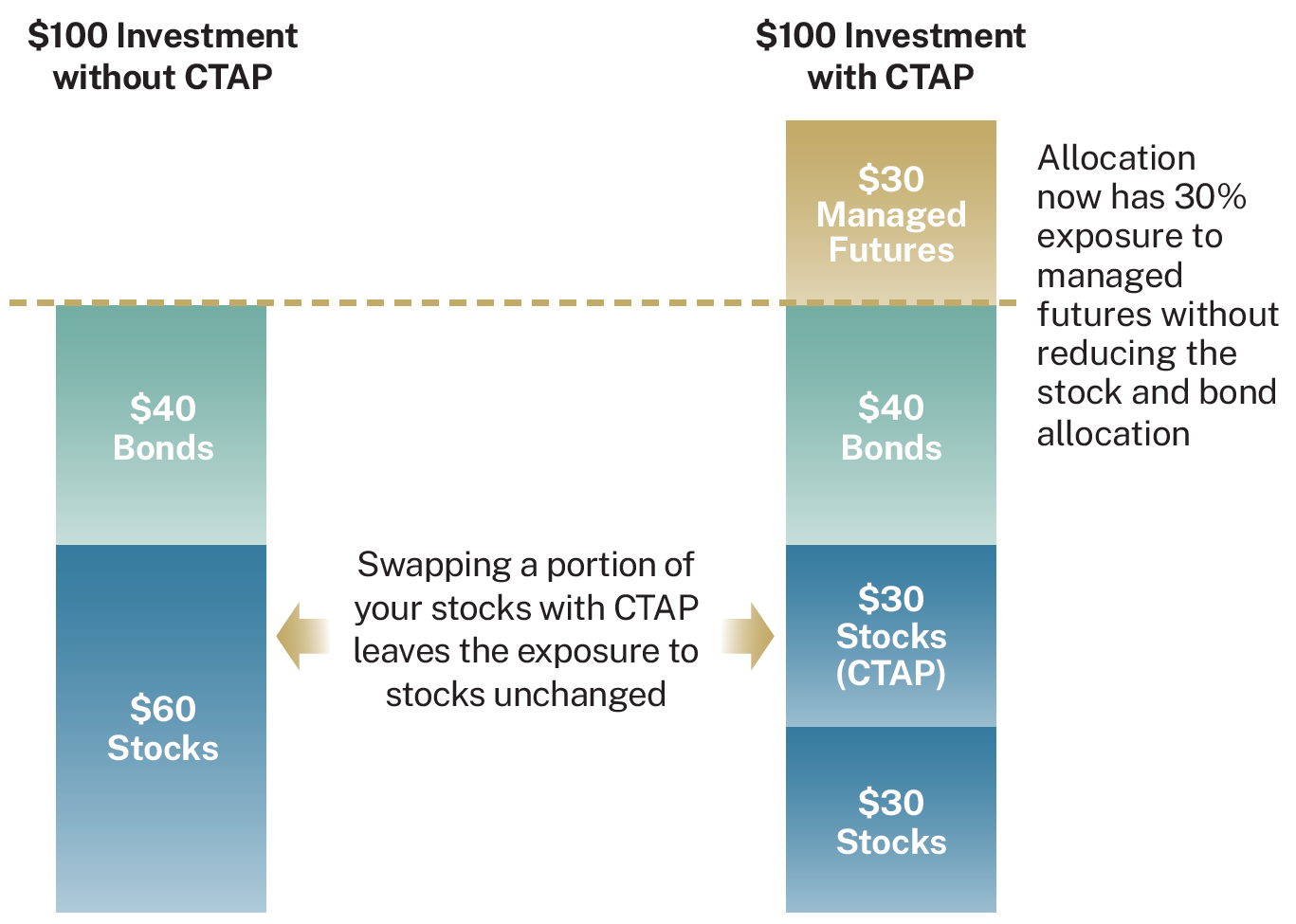

Suppose you start with a portfolio of $60 in stocks and $40 in bonds. If you were to replace, say, $30 of the stocks with CTAP, the $60 allocation to stocks would be unchanged, as would the $40 allocation to bonds. But the portfolio would have an additional $30 in managed futures without reducing any of the stock/bond exposure.

Using CTA to Obtain Managed Futures Exposure

CTAP’s managed futures exposure is obtained via total return swaps on the Simplify Managed Futures Strategy ETF (CTA). Total return swaps are derivative instruments that track the performance of an underlying asset – in this case, CTA.

CTA was launched in 2022 and has since then become one of the largest managed futures ETFs in the industry, with total assets over $1 billion as of January 31, 2026. CTA’s algorithm was built by its futures advisor, Altis Partners, a UK-based hedge fund with over 20 years of managing assets in the space.

Equity exposure is obtained via low-cost exchange-traded products plus a small amount of equity futures used to obtain the required amount of leverage.

Why Managed Futures?

If you haven't spent much time with managed futures, here's the elevator pitch: these strategies systematically follow trends across markets. The key difference from traditional investing? They have the potential to make money in both up and down markets by going long or short based on the trends they identify. What makes them valuable for portfolios comes down to three things:

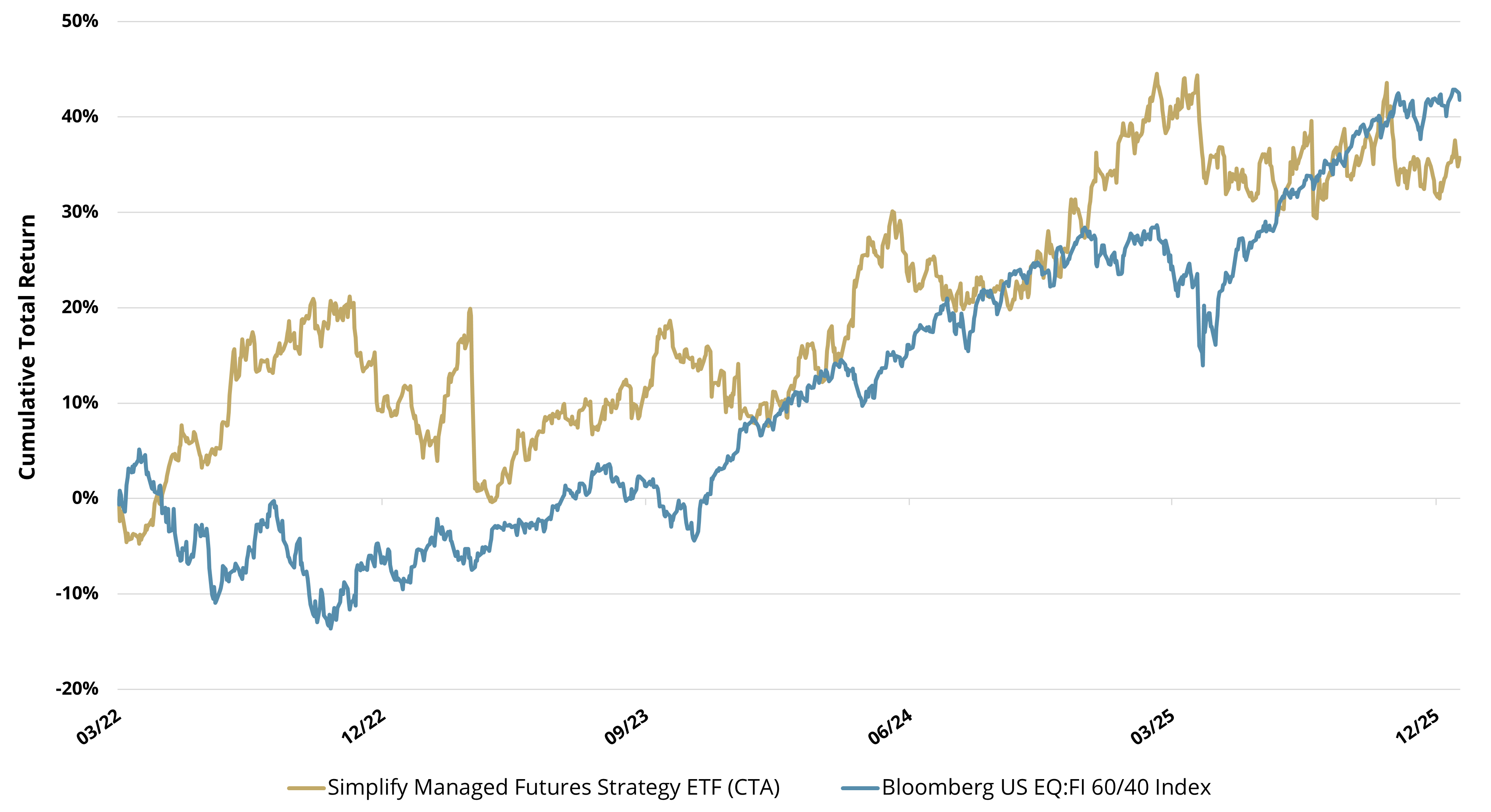

(1) They zig when stocks zag. Managed futures funds have historically had little to no correlation with stocks. Since its 2022 inception, CTA has had a slightly negative correlation with stocks. Yes, negative correlation! If you compare the total returns of CTA with the 60/40 portfolio, the zig-zag pattern is quite apparent.

CTA Has Acted as a Hedge to a 60/40 Portfolio

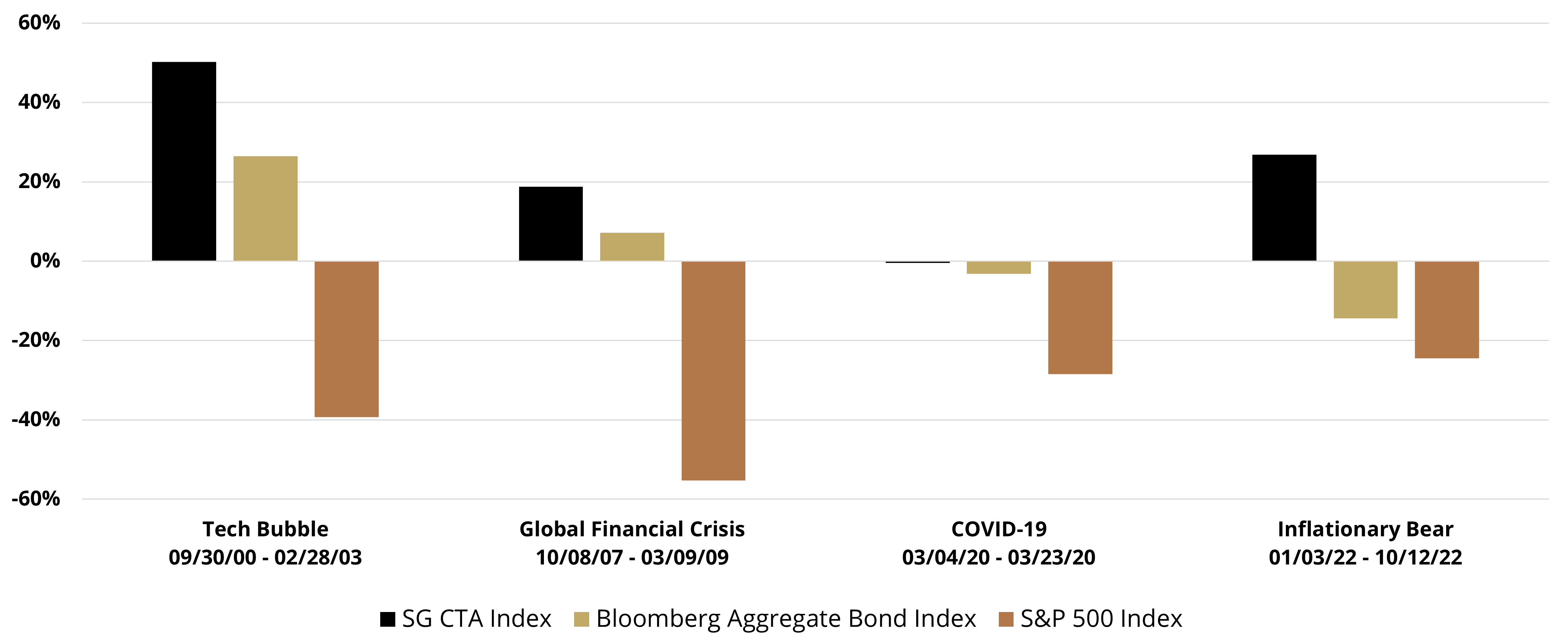

(2) They've shown up during crises. Look at the four major equity drawdowns since 2000. This chart compares the SG CTA Index - a common benchmark for managed futures – with the performance of stocks and bonds during these declines:

While past performance is not a guarantee of the future, managed futures funds have historically performed at their best when stocks are performing at their worst.

(3) They weathered the recent inflation surge better than bonds. The 2022 rate hikes caused a lot of pain for allocators who solely relied on bonds as their portfolio diversifier. Managed futures were one of the few things working, posting solid gains while many traditional 60/40 portfolios struggled.

How CTAP Can Solve Real-World Problems

- No more “what am I giving up?” conversations. Your clients keep full equity exposure while gaining diversification.

- Better odds of staying disciplined. This can be a significant behavioral advantage. Combining managed futures with stocks reduces line-item risk. It’s easier to stick with something when it’s not as visibly dragging on results.

- Built-in crisis hedge. The managed futures component can potentially cushion portfolios when equities are struggling.

- Professional execution. You’re not trying to manage futures positions, margin calls, or daily rebalancing. Everything is handled systematically.

- Benefits of the ETF wrapper, including daily liquidity and simple 1099 tax reporting.

- Potential tax benefits of using “bullet swaps”. Bullet swaps are a specific kind of total return swap in which the parties make a single payment at the maturity of the swap. By utilizing longer-term bullet swaps, there is potential tax efficiency by gains on the swaps being recognized as long-term capital gains upon expiration and not ordinary income.

What Are the Risks?

- When both components struggle, it hurts. If stocks and managed futures both decline, losses could be worse than just holding equities. The negative correlation is historical, not guaranteed.

- Managed futures can go through rough patches. Sudden, sharp reversals are their kryptonite. Whipsaw price action generates losses on both sides of trades. These periods can test patience. Simplify partnered with Altis Partners to deliver access to an institutionally robust hedge fund that seeks to minimize these sharp reversals.

- It's more complex than traditional equities. You need to explain this to clients and make sure they get it. If they don't understand what they own, you're setting up future problems. Simplify’s website (and this paper) seeks to demystify and educate, but we have plenty of experts in-house if you have more questions.

What to Expect

- Bull markets: The underlying equities will capture the equity upside. Managed futures might help, hurt, or do nothing depending on whether trends are present globally.

- Bear markets: This is where the design aims to shine. Equities will drop, but managed futures may generate positive returns if strong trends emerge. The combination can help to reduce the damage.

- Choppy, trendless markets: Both strategies might struggle. Stocks go nowhere; managed futures get. whipsawed. It's frustrating but part of the deal. This is when you earn your fee by keeping clients disciplined.

- Volatility: Expect day-to-day swings, but potentially smoother sailing than 100% equities when markets get rough.

Making It Work

First, size the position appropriately. Most advisors who use these strategies allocate 10-20%. Much less and it won't move the needle when you need it to. Much more and you're making a big bet, taking on more tracking error than your clients may be comfortable with.

Next, make sure you communicate the reason for owning the position. Your clients need to understand the dual exposure concept. Try using a simple version: "Think of it as two strategies working together—one tracking stocks, one potentially profiting from trends in any direction—in a single investment."

Once in place, you can set it and forget it. Establish your rebalancing bands and stick to them. Don't get cute trying to time when managed futures will work.

The Bottom Line

Capital efficient strategies aren't a magic bullet, but they solve a real problem: how to diversify portfolios without the behavioral baggage that comes with traditional alternative allocations.

The ability to maintain full equity exposure while adding managed futures changes the conversation with clients. Instead of asking them to accept lower potential returns for downside mitigation, you're offering both participation and diversification. When markets eventually get rough again (and they will), that downside mitigation may prove valuable.

GLOSSARY

Alpha: An investment strategy's ability to beat the market, or its "edge." Alpha is thus also often referred to as “excess return” or the “abnormal rate of return” in relation to a benchmark, when adjusted for risk.

Bloomberg US EQ:FI 60:40 Index: Designed to measure cross-asset market performance in the US. The index rebalances monthly to 60% equities and 40% fixed income. The equity and fixed income allocation is represented by Bloomberg US Large Cap (B500T) and Bloomberg US Agg (LBUSTRUU) respectively.

Derivative: A type of financial contract whose value is dependent on an underlying asset, group of assets, or benchmark.

Managed Futures: An investment where a portfolio of futures contracts is actively managed by professionals. Managed futures are considered an alternative investment and are often used by funds and institutional investors to provide both portfolio and market diversification.