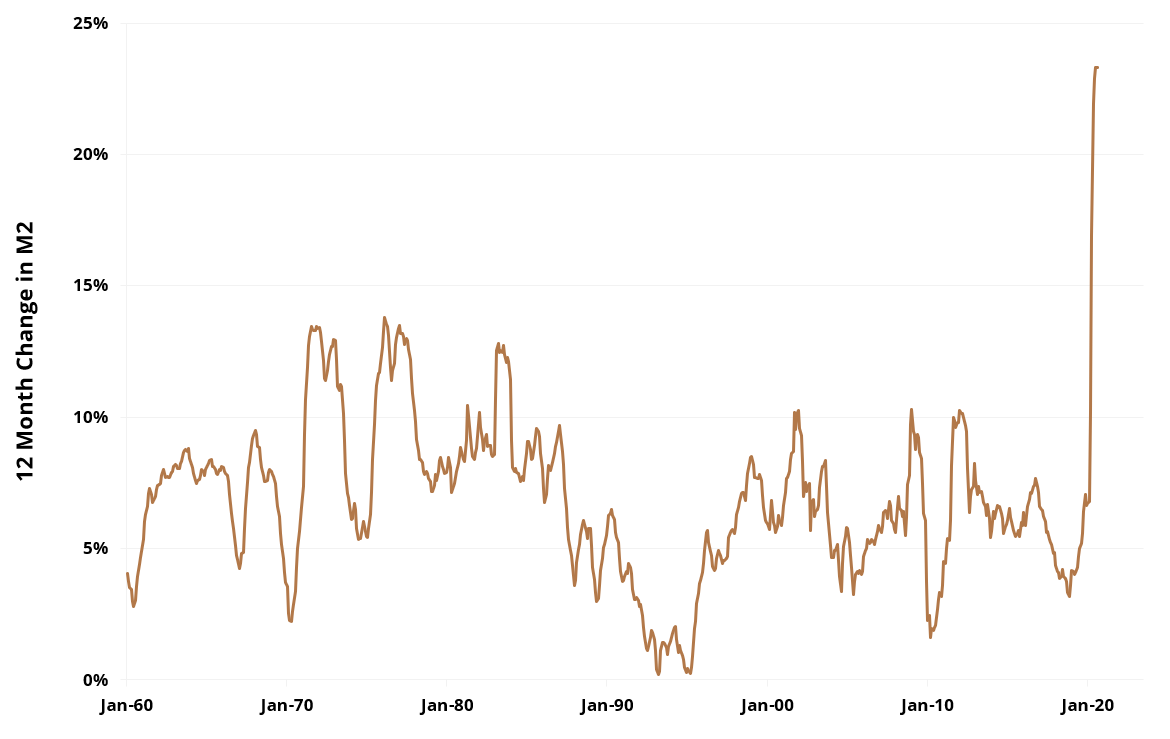

While some observers, focusing on the dramatic demand destruction globally, believe that disinflation or deflation is more likely, we can generously suggest that others disagree. Arguing in favor of a more inflationary possible outcome, some point to the supply-side destruction and the decline in free and open trade policies; even more concerning to us is the potential that the combination of awe-inspiring monetary and fiscal stimulus could provoke an inflationary outcome that would be especially difficult to manage in an environment of weak real growth. Figure 1 shows the year-over-year growth in the M2 money supply, which is not only without U.S. precedent (including in the inflationary 1970s) but also is at a level never before seen in any country that did not experience higher inflation than the U.S. presently enjoys.

Figure 1: Year-Over-Year Growth in M2 Money Supply (1/31/1959-8/30/2020)Source: Federal Reserve. Calculations by Simplify Asset Management. The results are NOT an indicator of future results. Additional information regarding the construction of these results is available upon request. PLEASE SEE FULL DISCLOSURES BELOW.

Regardless of which camp – inflation or disinflation – one falls into, it is hard to argue that the possibility of higher inflation should be dismissed. This then naturally leads many to contemplate the impact higher inflation could have on equity-dominated portfolios. In this blog post we will review how inflation impacts equities and provide advisors with a simple and clear framework for how different inflationary outcomes could effect equity-centric portfolios.

A Primer on Inflation's Impact on Equities

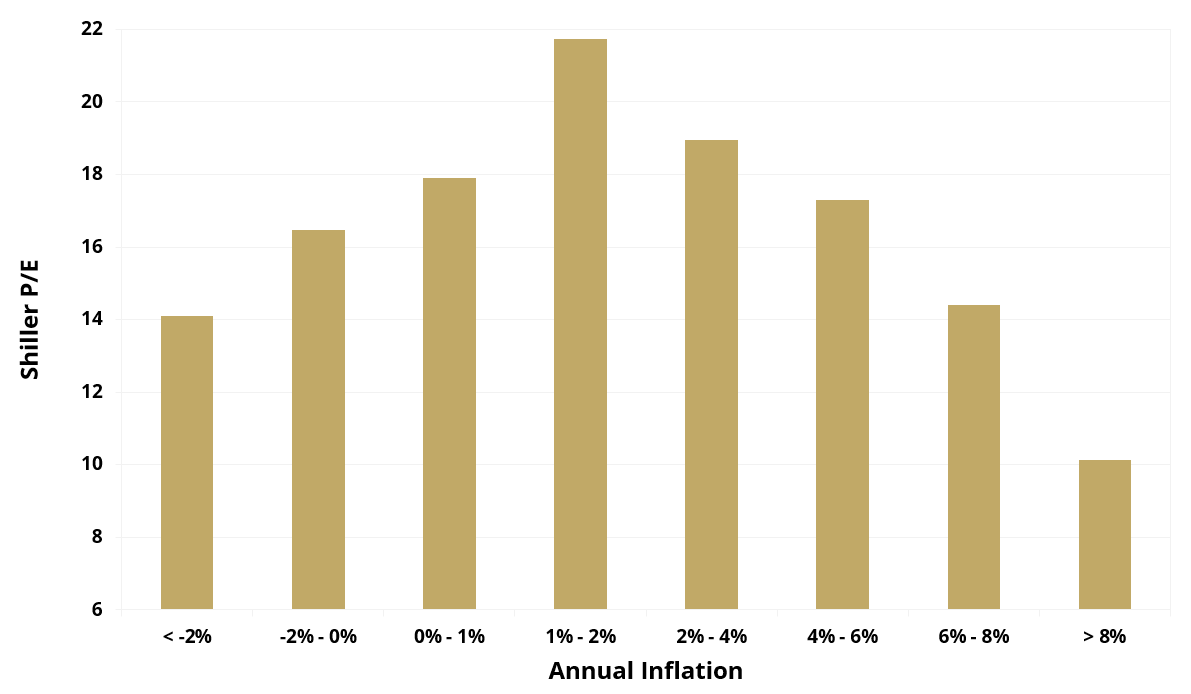

Rising inflation is good for corporate earnings, in nominal terms. If revenues double, and expenses double, then earnings double. But at the same time, rising inflation also tends to decrease the multiples attached to those earnings, and this has been well-known at least since the 1970s. Figure 2 shows this tendency for multiples to be highest when inflation is low and stable, and lower as actual inflation deviates from that Goldilocks zone.

Figure 2: Shiller P/E vs Annual Inflation (1881-2019)Source: Robert J Shiller, US Bureau of Labor Statistics, Enduring Investments. Calculations by Simplify Asset Management. The results are NOT an indicator of future results. Additional information regarding the construction of these results is available upon request. PLEASE SEE FULL DISCLOSURES BELOW.

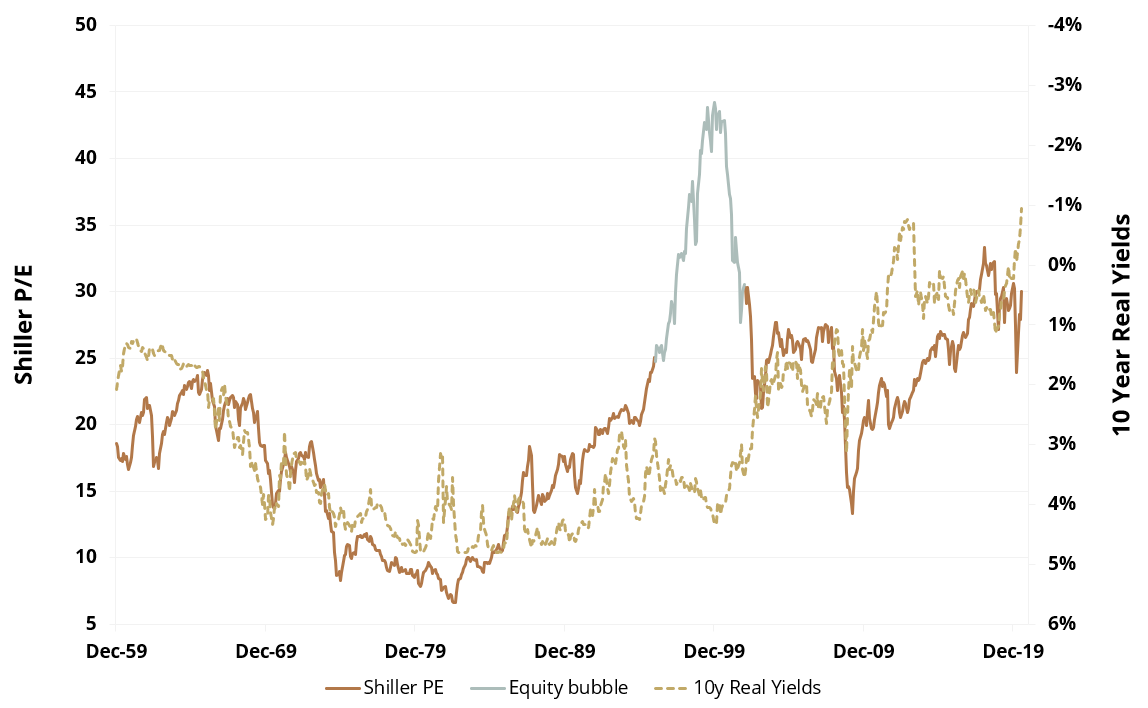

However, a more nuanced analysis actually connects multiples to real interest rates. The intuition is that a business is a real asset, for precisely those reasons noted above: rising inflation tends to increase corporate earnings in nominal terms. But if this is so, then it would be appropriate to discount corporate earnings by real interest rates, so that lower real interest rates would be associated with higher multiples, and vice-versa. In fact, since higher inflation and higher real rates are correlated – when inflation goes up, so do real interest rates, on average – this is likely the reason that multiples decline when inflation goes up per Figure 2: because the real discount rate also rises. Empirically, as shown in Figure 3, there is a pretty convincing relationship between longer-term real yields and multiples, at least outside of bubble periods.

Figure 3: Shiller P/E vs 10 Year Real YieldsSource: Robert J Shiller, Bloomberg, Enduring Investments. Calculations by Simplify Asset Management. The results are NOT an indicator of future results. Additional information regarding the construction of these results is available upon request. PLEASE SEE FULL DISCLOSURES BELOW.

What Today's Level of Stimulus Could Mean for Equities

So higher inflation is traditionally good for nominal earnings but bad for the stock market as a whole because of the higher (real) discount rate that typically accompanies such inflation. But is it really fair in today’s markets to expect that if inflation picks up then real yields will necessarily pick up as well, enforcing multiple compression that would hinder equities? At the time of this writing, 10-year real yields are at an all-time low of approximately -1%, which would seem to offer little encouragement that drastically lower real yields are likely, especially if inflation rises.

Today however there is a relatively simple case to be made that real interest rates could actually decline substantially further, enabling equities to rally alongside an uptick in inflation. With the Fed Funds rate at zero, there has been discussion within the Federal Reserve about additional tools to conduct monetary policy if additional stimulus is perceived to be required. One of these is yield curve control (YCC), which was actually implemented in the United States during World War II. (A good explanation of Yield Curve Control is offered by the St. Louis Fed here). Under YCC, the Fed caps the interest rates of longer-term securities, and potentially the entire yield curve, by offering to buy as many bonds as necessary to maintain those caps. Suppose that the Fed implements such a policy. In that case, if inflation rose while nominal rates were capped then it would force real rates to fall. For example, currently nominal 10-year interest rates are near 0.75%, and with the market expecting 1.75% inflation over time that makes real yields – reflected in TIPS – the -1.00% mentioned earlier. If inflation rose to 3.75%, and the 10-year nominal rate was constrained by the Fed to stay at 0.75%, then real yields would be forced to decline to -3.00%. That would imply a massive rally in TIPS, and if investors react to lower real interest rates in the way they traditionally have, it would also cause a massive rally in the equity market.

Parting Words

Recent stimulus measures have raised the specter of significant inflation, and alongside that the possibility of an inflation-driven equity boom. While outsized inflation historically leads to lower multiples, the prospects of YCC have raised the possibility of a divergence from that historic norm, into an environment of inflation accompanied by multiple expansion. For anyone worried about an inflation-driven equity boom, just keep a careful eye on inflation and the Fed's policy on YCC and real yields.