Investors are increasingly concerned about rising interest rates, and the reality that higher rates can have adverse financial consequences for portfolios and businesses. Since the magnitude and timing of rate moves is uncertain, the question of what to do about it is both critically important and very hard to answer.

One solution is to reduce or eliminate exposure by shorting rates. This comes with the high cost of losing potential income and the diversification benefits of fixed income exposure. The ideal solution is a conditional, options-based hedge, that only reduces exposure when rates move against your position, but these can be expensive and hard to manage, and subject to path dependency if not carefully selected and constructed.

In this blog we present an alternative solution -- an optimized interest rate hedge that utilizes long-dated over the counter (OTC) swaption contracts. With the proper selection of swaption parameters, one can create a conditional hedging profile that is highly convex and robust across a broad range of rate paths, with a low-cost of ownership.

Trimming vs Insurance

One interest rate hedging approach is to reduce or remove the exposure altogether. For investors, this can range from shortening the duration of a fixed income portfolio, taking it to cash, to the extreme of shorting fixed income securities through derivatives markets. Businesses and institutions reliant on low-cost financing typically lock up current and future financing through the use of commitments and derivatives. These approaches solve one problem, reducing losses associated with a rate rise but introduce additional problems. For investors, the income and gains generated by exposure to rates if rates stay the same or decrease is lost. For businesses or institutions, the losses associated with locking in financing for projects that may not be realized or may be realized in a lower rate environment can also be very costly.

Even large and sophisticated market participants such as Harvard struggle with this decision. Harvard’s experience during and shortly after the financial crisis is instructive as an investor, through its endowment, and as an institution that is a major participant in debt markets, as part of its university operations.

In the early 2000’s Harvard University decided to undertake a major expansion into the Boston neighborhood of Brighton, just across the river from its main campus in Cambridge. Their plan -- develop several large parcels of land they had acquired in Brighton to create a multi-billion-dollar world-class science and biotechnology campus. In addition to securing the property, Harvard also committed to fixed rate borrowing to finance the project, at a rate that seemed attractive at the time. Advance the calendar a couple of years and we find ourselves in the midst of a financial crisis which dramatically cut the value and liquidity of many of Harvard’s endowment assets, reduced the ability of its donor community to provide meaningful gifts, and otherwise stressed the university’s operating finances as grants dried up and demand for student financial aid increased.

On the endowment side, Harvard had reduced exposure to fixed income assets in favor of riskier and less liquid positions. The fixed income positions they abandoned prior to the financial crisis would have provided both a powerful diversification benefit (bonds rallied during the crisis in response to central bank action) as well as an important source of liquidity. Because Harvard’s endowment asset allocation was short on duration and illiquid, it found itself having to liquidate many of its positions at distressed prices. After they decided to indefinitely postpone the Brighton development project, the commitments they made to borrow fixed amounts at a fixed rate, eventually ended up costing Harvard about $1.25 billion to unwind.

Given this fact set, a conditional hedge that protects against rates increasing when one needs it but is less reactive to a rate decrease would be most desirable. Essentially, what we have just described is an option, a position that increases its sensitivity to the underlying risk factor as the risk driver increases and decreases its sensitivity as the risk driver decreases. As discussed in our other blogs, this type of favorable variable sensitivity is known as positive convexity. Had Harvard purchased an option on rates that paid them if rates went up instead of committing to borrow at what turned out to be higher than market rates, all they would have lost is some of the option premium they paid to purchase the option. This could have easily turned out to be a 10th of the cost incurred to unwind their financing and swap positions.

Having identified options as a potentially powerful tool, the question then becomes which options or configuration of options offers the most desirable profile. In making this determination we want to consider how the basic features of an option (market, underlying, term to expiry, strike) interact and relate to the risk management problem. In the sections that follow we take each of these features in turn to parse out an optimal option hedge for rising rates.

Why OTC Options?

When we examine the options markets available to those wanting to hedge US dollar interest rate risk we see both well-developed listed and OTC markets. However, within listed options we see liquidity that is available to a limited palette of underliers; Eurodollar futures and US Treasury futures with liquidity that extends for a fairly limited set of terms to expiry inside of 1 year.

If what we are concerned about are large rate changes that may take years to develop, short term-to-expiry options are not the appropriate tool. For instance, let’s consider a scenario for the 10-year US treasury where it ends up yielding more than 4% (yielding 1.62% as of April 30, 2021) after 3 years pass. Someone using short term options to hedge this outcome would want to roll through a series of 12 6-month options held for 3 months each to hedge this risk. It’s not hard to see that the path taken in getting from 1.5% to 4% or more on the treasury yield would have a material impact on the cost and ultimate effectiveness of the hedge. For this scenario, a much more effective and predictable hedge would be one that involves a single option, with three or more years to expiry and a strike of around 4%.

This type of option, while not available in listed markets, is readily available in liquid, deep and frequently traded OTC markets. These markets are typically inhabited by banks, broker dealers, insurers, corporations and other institutional participants with very specific needs that help create the full palette of terms available. In terms of size, these markets are in aggregate larger than the listed markets when measures of exposure such as aggregate DV01 (sensitivity to changes in rates) and Vega (sensitivity to changes in implied volatility) are used as yard sticks. By accessing the full palette of terms to expiry, strikes and underlying rates available in the OTC market, one can expressly build a predictable, low cost of ownership hedge to a rapid rise in interest rates. In the section that follows we walk the reader through precise underlying rate, strike, and expiry that we believe will build the most optimal interest rate hedge.

Optimal Swaption Selection for Hedging Rates

We believe the optimal hedge for the specter of rising rates is a 7y into 20y payer swaption with a strike of 4.25%. This option is in the money if on its expiration date, 7 years from now, the 20-year swap rate is greater than the strike of 4.25%. Here it is important to note that the underlying swap for this option is a highly liquid plain vanilla centrally cleared swap with deep two-way liquidity. The option can be viewed as a call on the pay fixed swap rate, or equivalently, as a put on a 20-year bond with a fixed rate of 4.25%. This hedge position takes advantage of several features of today’s volatility surface and rate term structure to provide a low cost of ownership over a multi-year horizon. Below we take each of these features in turn.

Rate Term Structure

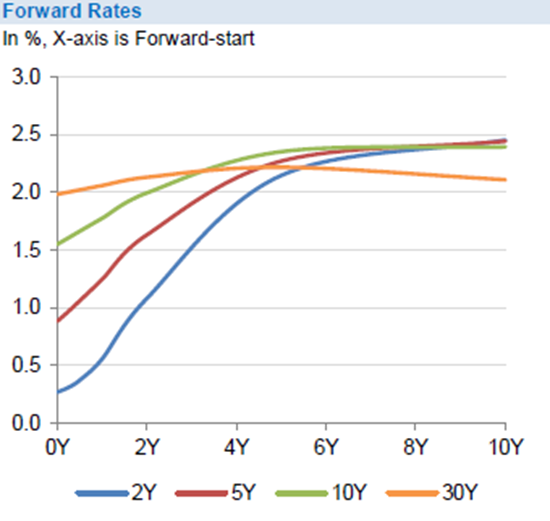

Options are priced in the forward market, with the result that changes in the forwards, as they roll to spot, affect the value of the option. When we look at the term structures for rates, as shown in Figure 1, we see that they rise sharply for shorter terms to expiry and then flatten out and become slightly downward sloping when you look far enough out. For shorter terms to expiry (inside of about 5 years), on shorter maturity rates (Maturities inside of 5 years), the passage of time has the forwards decreasing as the calendar advances toward the expiry of the option. The opposite is true for longer maturity rates with longer terms to expiry, where the term structure is flat to upward sloping. For these longer maturity rates, farther out on the term structure of rates, the passage of time has options on rates rolling favorably. Hence the optimal term choices for positive roll on the term structure are both a long term to expiry, that is greater than 5 years and a long dated underlying rate, that is greater than 10 years.

Figure 1 – Rate Term StructureSource: Morgan Stanley DSP

Volatility Term Structure

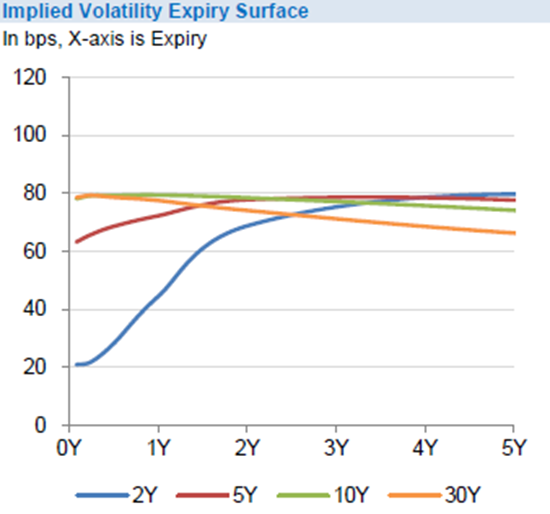

For volatilities we see a pattern very similar to the one observed for the forward rates term structure. The annualized implied volatility on rates with 5 or fewer years in maturity grows rapidly and then stabilizes for options with 4 or more years to expiry. For longer maturity rates, the implied volatility per unit of time decreases as the option term increases. In this sort of pricing environment, the options on longer maturity rates roll up the vol surface in a way that can substantially offset time decay, another key justification for long terms to expiry and long dated underlying rates.

Figure 2 – Volatility Term StructureSource: Morgan Stanley DSP

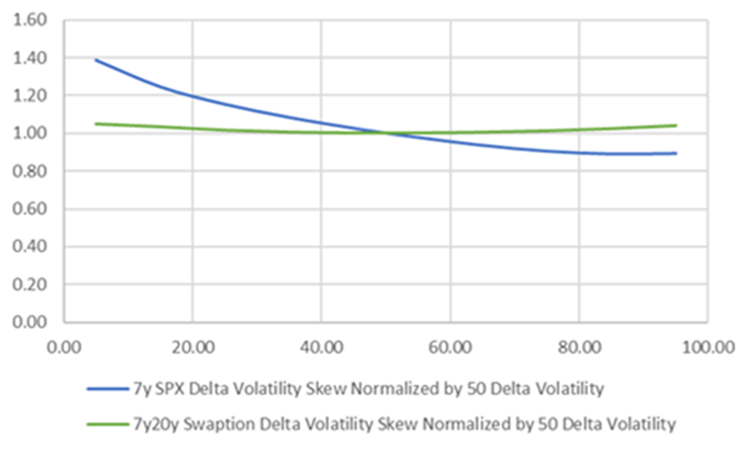

Volatility Skew

For many asset classes, protection against sell offs is priced at a significant premium to at the money options. Figure 3 below shows a comparison between the skew priced into long dated equity options (Blue Line) and long dated swaptions (Green Line). This comparison shows that for out of the money puts, say at a 10% Delta, the volatility premium demanded by the market is roughly 10 times greater for equity protection than it is in interest rate options markets. This stark difference creates the opportunity for those wanting to hedge against large sell offs in the bond market to own out of the money protection at a much lower cost, justifying our enthusiasm for a deep OTM strike near 4.25%.

Figure 3 - Volatility SkewSource: Morgan Stanley DSP

Payoff Expectations

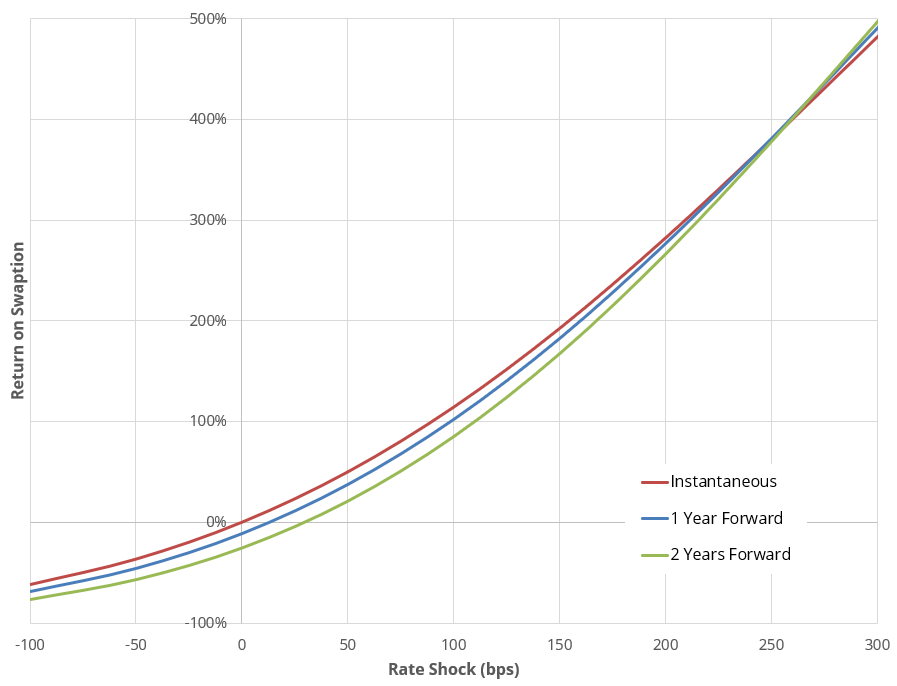

So, we have constructed a rate hedge that we theoretically expect to be highly convex while simultaneously having a low cost of carry. Let’s now take a moment to see if the payoff of such a trade indeed satisfies both requirements. Figure 4 shows a simulation of a single 7y20 swaption as a function of rate changes and the horizon over which these rate moves happen. This simulation does not represent any investment strategy in existence, but rather is meant to show the dynamics of this particular swaption. Also note that in this simulation, volatility of rates is assumed to stay constant, which in general would be a tailwind to the option if rates go up and be a headwind to the option as rates go down. As you can see, we certainly see a very convex payoff of the options, with a better than 5:1 ratio of upside to downside. Additionally, we only see a roughly 10% drop in option value after 1 year when rates stay the same, an attractive cost for the upside convexity just discussed.

Figure 4 – Swaption Payoff Over Various HorizonsSource: Calculations by Simplify Asset Management. The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Hypothetical strategies and indices presented are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request. PLEASE SEE FULL DISCLOSURES BELOW.

Parting Words

Rising rates can pose serious problems to portfolios. Although there are many approaches to managing the risks that rising rates bring, only options-based solutions provide an effective hedge in a world where the timing, direction and magnitude of rate changes has substantial variability. Among options-based hedges, long dated swaptions provide an effective solution with an exceptionally low cost of ownership and robust asymmetric protection across a broad range of scenarios.