Low interest rates and specifically, zero interest rate policy (ZIRP) conducted by monetary authorities, have fundamentally altered the expected return of bonds, as well as their ability to protect portfolios. With rates near all-time lows investors are currently challenged by the opportunity cost of remaining invested in the asset class. In our recent blog “Risk Management is More Than Just Diversifying Into Bonds”, we provided an alternative framework to the traditional 60/40 portfolio that uses equity index put options to help protect equity-focused portfolios. And in our blog titled “Convex Equity Positioning When Bond Expectations Are Low”, we explored more precisely how portfolios should optimally pivot from bond-focused protection to option-focused protection given extremely low bond yields. But both of these reports were focused on the opportunity cost associated with low bond yields and didn’t focus on another elephant in the room, which is whether bonds can protect portfolios during times of stress as well as they have historically given their low yield starting point. Bonds have provided a level of drawdown protection during recent extreme market drawdowns, but has this always been the case and is it sustainable in a near-zero rate environment?

Bond Protection When Yields Are Low is Limited

To help answer this question we will consider the behavior of the U.S. 10-year Treasury, a conservative bond proxy relative to a more diversified (and credit-focused) bond portfolio. As of the submission of this piece, the U.S. 10-year Treasury yield (TNX) is struck at 0.94%, near an all-time low and the intuitive lower bound of zero. For reference, TNX yielded a record-high 15.82% in September 1981. Though a move from one extreme to the next has been relatively gradual and generally profitable for bond investors, current market participants looking to deploy capital in fixed income are facing the worst forward-looking return potential and highest average duration for the asset class in modern market history. If we presuppose that interest rates have a hard floor of 0%, there is not much room between such a floor and a reversal in which rates begin trending higher, giving a hard cap to the potential protection that Treasury bonds can provide portfolios.

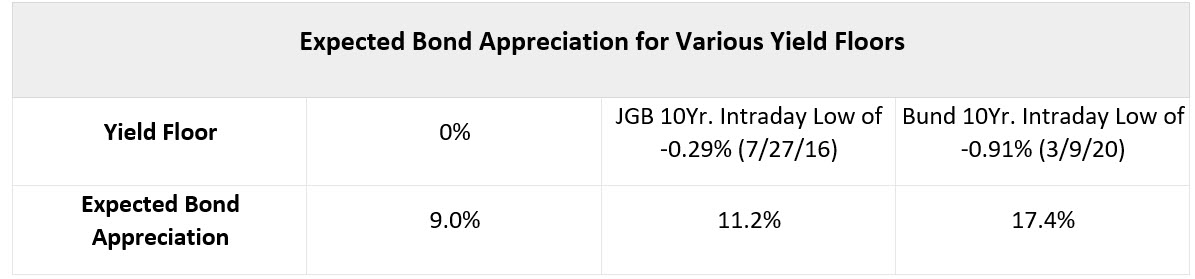

But is a concrete interest rate floor of zero a settled fact? While negative rates have yet to materialize on the middle-to-far end of the Treasury yield curve, the 4-week T-Bill entered negative territory for the first time in March of 2020, effectively puncturing the notion of a zero lower-bound in U.S. fixed income markets. Negative rates are the norm in other developed bond markets including Germany (bunds) and Japan (JGBs), with the former government’s yield curve trading entirely below 0%. How might these real-world scenarios play out in U.S. fixed income markets? Figure 1 displays the limited potential for bond upside (aka diversified portfolio downside protection) of 9.0% on a 10-year U.S. Treasury bond provided an interest rate floor of 0%. Further, the table incorporates negative interest rate scenarios using the intraday all-time lows for both JGBs and bunds. It is worth noting that negative yields can push duration beyond its established ceiling due to the expectation that, if held to maturity, one would not recoup the full par value of the investment. For our calculations, we used a maximum duration of 10 years.

Figure 1: Examining the Potential Drawdown Protection of a 10-Year Bond Yielding 0.94%

(as of 12/08/2020)Source: Federal Reserve/Dow Jones/Wall Street Journal. Calculations by Simplify Asset Management. The results are NOT an indicator of future results. Additional information regarding the construction of these results is available upon request. PLEASE SEE FULL DISCLOSURES BELOW.

We Have Already Seen Bonds' Ability to Protect Wane

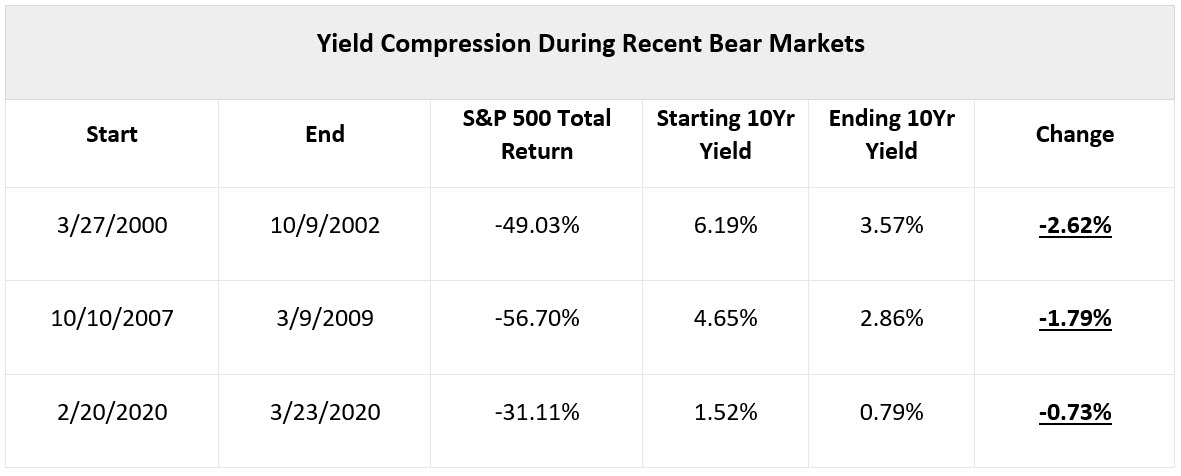

In recent decades, the 10-year Treasury has, by and large, delivered its expected end of the bargain during equity market selloffs. Treasury yields have decreased (as related bond/index prices have increased) during each of the five long-term bear market declines since 2000. However, yield compression over the past two decades has not only increasingly reduced the term premium for the asset class after each bear market event but also has produced noticeably smaller benefits in terms of price appreciation for the respectively held bonds. In Figure 2, we show how a bond portfolio with a duration of 10 years gained approximately 26.2% of price return during the 2000-2002 bear market, whereas a similar portfolio only gained about 17.9% during the 2007-2009 bear market. During the COVID crash of March 2020 in which the S&P 500 Index fell over 30%, such a portfolio returned a mere 7.3%, continuing this disappointing trend as the diminished margin between yields and the theoretical zero lower-bound became even more condensed.

Figure 2: Bear Markets in U.S. Equities and the Respective Impact on 10-Year Treasury Yields (3/27/2000 – 3/23/2020)Source: Koyfin. Calculations by Simplify Asset Management. The results are NOT an indicator of future results. Additional information regarding the construction of these results is available upon request. PLEASE SEE FULL DISCLOSURES BELOW.

And Yields Can Even Rise During Drawdowns

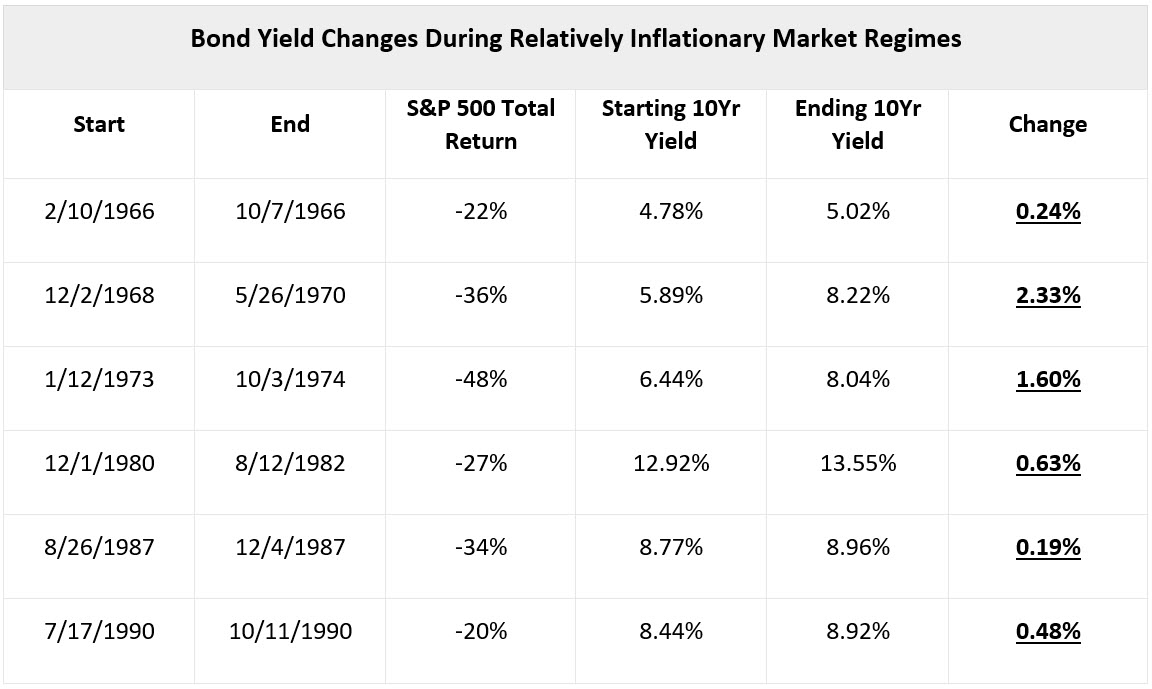

Matters are in fact worse, as even a Treasury bond portion of an asset allocation portfolio has not always served as a ballast against equity market stress. Figure 3 shows equity bear market drawdowns that have occurred in environments with higher relative inflation than the present, coinciding with increases in yields that were destructive toward the fixed income side of an asset allocation portfolio when protection was most desired. In a worst-case scenario for asset allocators, the bear market of 1968-1970 resulted in an increase in yields from 5.89% to 8.22% - equating to a whopping 23.3% decline on a 10-year duration Treasury bond. As we dwell near the lower extreme of historical bond yields, a bit of historical context is a sobering reminder that market regimes are cyclical in nature. How much room is left to run in this bond bull market, and what are the potential costs for an asset allocation strategy should rates rise instead of decline during a catastrophic market event?

Figure 3: Bear Markets in U.S. Equities and the Respective Impact on 10-Year Treasury Yields (2/10/1966 – 10/11/1990)Source: Koyfin. Calculations by Simplify Asset Management. The results are NOT an indicator of future results. Additional information regarding the construction of these results is available upon request. PLEASE SEE FULL DISCLOSURES BELOW.

Parting Words

Low interest rates are an increasingly burdensome opportunity cost for bond holders as yields linger near zero. But less discussed, and maybe even more problematic, is the fact that low yields will ultimately limit the amount of protection even the most conservative of bonds can offer. Even worse, a strong inflationary environment can render such bonds useless from a protection standpoint, a scenario we may indeed not be too far from. With direct hedges like put options, there is no need for investors to drag on their returns or risk the failure of correlation hedges like Treasury bonds during low rate or inflationary macro environments.