In our last blog post we reviewed how put options could potentially be used to limit downside risk of an equity investment. Specifically, we showed that a hypothetical portfolio of 98% S&P 500, supported by a 2% annual investment in an advanced put overlay, had drawdowns in line with a 60/40 portfolio (see Figure 1 for a summary of those results). The post’s punchline was then inevitable: if you have serious doubts about bond returns over the next couple decades then an equity + put strategy could make a lot more sense for capital protection than the classic equity + bond diversification paradigm. Admittedly though, this intuitive conclusion presupposed that drawdown control was the sole portfolio benefit of bonds, but in fact we know people also rely on bonds to help control portfolio volatility. Additionally, we didn’t provide any hard numbers on how changing bond return expectations would actually tilt optimal portfolios in favor of the convex equity exposure. To address both open issues we will introduce the common mean-variance framework for building client portfolios, and we will then see how lowering bond return expectations precisely changes the optimal client exposure to equities with downside convexity.

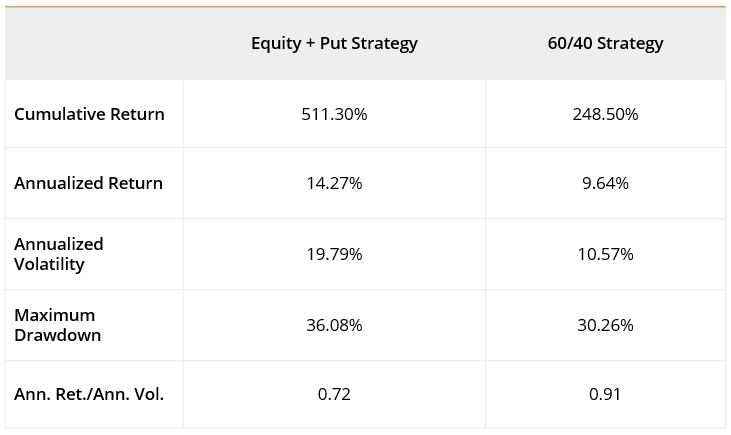

Figure 1: Hypothetical Equity + Put Strategy vs Hypothetical 60% SPY/40% TLT Strategy - Hypothetical Returns from 1/1/07-7/31/20Sources: QuantQuote & Options Price Reporting Authority. Calculations by Simplify Asset Management. The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Hypothetical strategies and indices presented are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request. PLEASE SEE FULL DISCLOSURES BELOW.

Risk Tolerance Portfolios with Mean-Variance Optimization

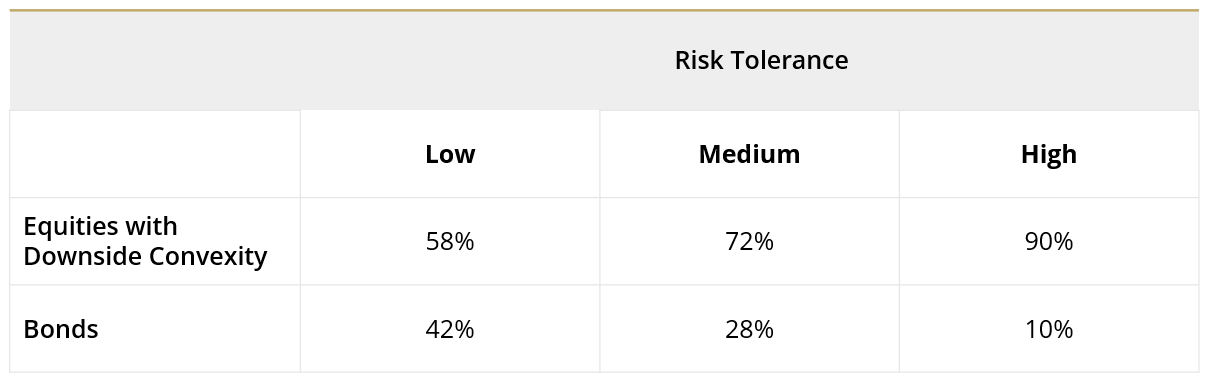

While capital protection may intuitively feel like the primary focus of any risk management paradigm, it is actually more the exception than the rule in wealth management today; advisors typically build portfolios that maximize return while minimizing volatility, which does not explicitly focus on drawdown protection. In this framework an advisor will typically get to know their client’s risk appetite and bin them in one of three risk tolerance levels: low, medium, and high. For each risk tolerance bucket an asset allocation is then created that maximizes the portfolio’s expected return while minimizing the volatility. Figure 2 shows the optimal mean-variance portfolios for three standard risk tolerance buckets when investing in a mix of equities with downside convexity and bonds (a constant maturity 30 Year Treasury bond), assuming hypothetical return, volatility, and correlation data from 1/1/2007-7/31/2020. As you would expect, the equity allocation rises as risk tolerance increases. (One may be a bit surprised by how high the 72% allocation to equities is in the medium risk tolerance bin, but note that with a passive equity exposure that bin would be invested in 58% equities with the given capital market assumptions, very close to the 60% paradigm in the 60/40 portfolio.)

Figure 2: Optimal Mean-Variance Portfolios for Three Risk Tolerance Levels (based on data from 1/1/2007-7/31/2020)Sources: QuantQuote & Options Price Reporting Authority. Calculations by Simplify Asset Management. The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Hypothetical strategies and indices presented are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request. PLEASE SEE FULL DISCLOSURES BELOW.

The Impact of Lower Bond Return Expectations

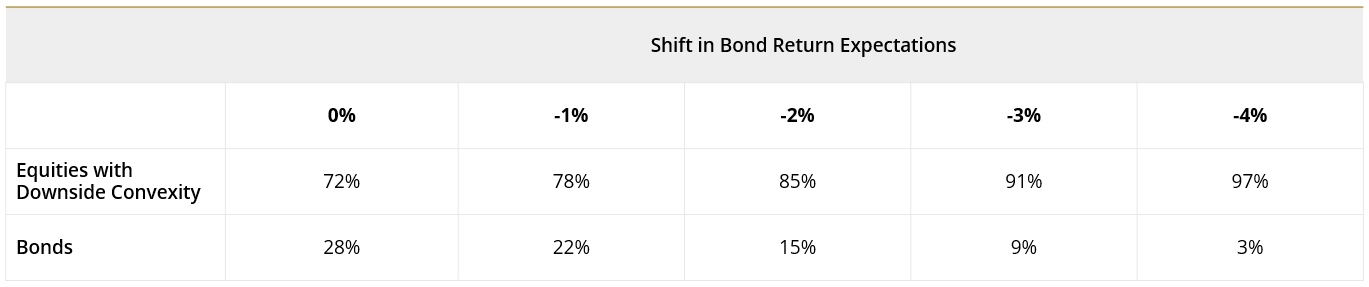

Now that we have a mean-variance framework established for 3 risk tolerance bins, we can now precisely analyze the effect of lowering bond return expectations on optimal portfolios, and see if a dim view on bonds could in fact justify fully swapping a bond/equity allocation for equities with put protection. To keep things simple we will only analyze how the optimal equity/bond allocations evolves for the medium risk tolerance portfolio as a function of bond expectations. Figure 3 shows the optimal mean-variance allocation between bonds and the equity + put strategy as a function of the annual bond reductions one expects relative to the bond return experienced in-sample from 1/1/2007 to 7/31/2020. Now the average bond return during this period was approximately 7% annually, in line with the strong annual bond returns of approximately 8% seen during the bull bond market realized over the last 50 years. Hence in Figure 3 we are showing optimal portfolios as bond return assumptions go from 7% annually all the way down to 3% annually, a very realistic possibility given where the current 30 year Treasury yield is today (1.5%) and how strongly bond returns correlate to starting yields.

Hence we see that in the context of challenged bond expectations, a complete swap of the 60/40 paradigm for convex equities is indeed conceivable in a risk tolerance portfolio framework if bond returns are roughly cut in half from the levels realized over the last 50 years.

As you can see in Figure 3, reduction of the expected return for bonds towards current yield levels quickly moves allocation from bonds to equities with convex downside protection. Hence we see that in the context of challenged bond expectations, a complete swap of the 60/40 paradigm for convex equities is indeed conceivable in a risk tolerance portfolio framework if bond returns are roughly cut in half from the levels realized over the last 50 years. Hence our downside-focused conjecture in our previous post, whereby one could use equity downside convexity as a primary risk mitigator, applies equally as well in a modern portfolio theory setting when bond returns are expected to lag recent strong performance by about half, a very realistic possibility given where interest rates are today.

Figure 3: Optimal Mean-Variance Portfolio for Medium Risk Tolerance as a Function of Annual Bond Return Reduction (based on data from 1/1/2007-7/31/2020)Sources: QuantQuote & Options Price Reporting Authority. Calculations by Simplify Asset Management. The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Hypothetical strategies and indices presented are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request. PLEASE SEE FULL DISCLOSURES BELOW.

Parting Words

In our previous blog post we intuitively declared that equities with built-in options-based drawdown controls could potentially be used as a replacement to the 60/40 paradigm, especially in a low rate environment. In this post we went beyond intuition and more rigorously analyzed how mean-variance optimal portfolios with convex equities and bonds evolved as a function of bond return expectations. We saw that if one cuts bonds return expectations roughly in half from those realized over the past 50 years, a complete swap from the standard equity + bond paradigm and into a downside control paradigm via equities with downside convexity is indeed optimal.